WEEKLY TREND REPORT

SUNDAY, JUNE 27, 2021

WEEKLY MARKETS RECAP

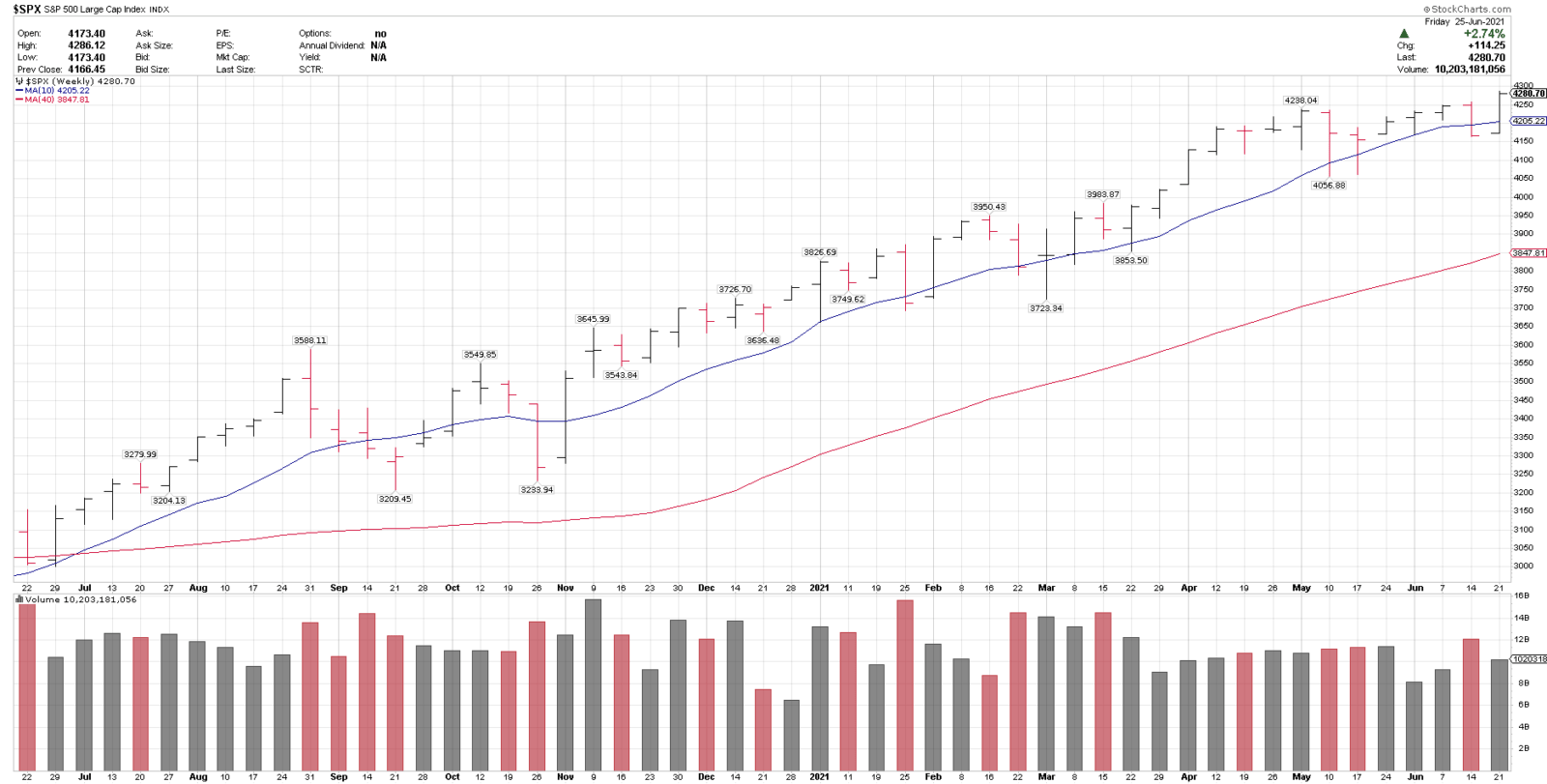

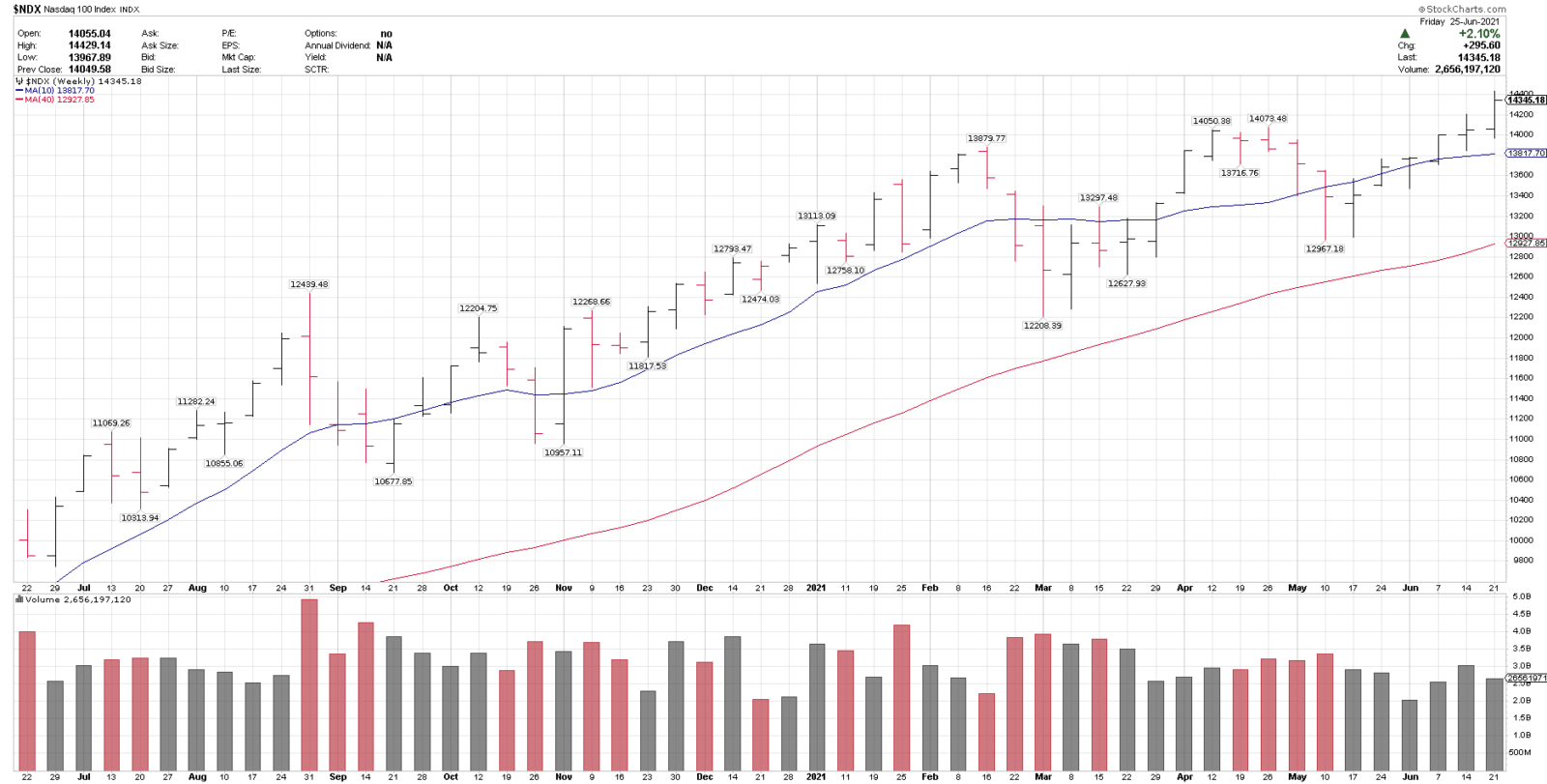

- Nasdaq 100 (NDX, QQQ) and SPX made new all time intra-day and weekly closing highs.

- Nifty made a new weekly closing high.

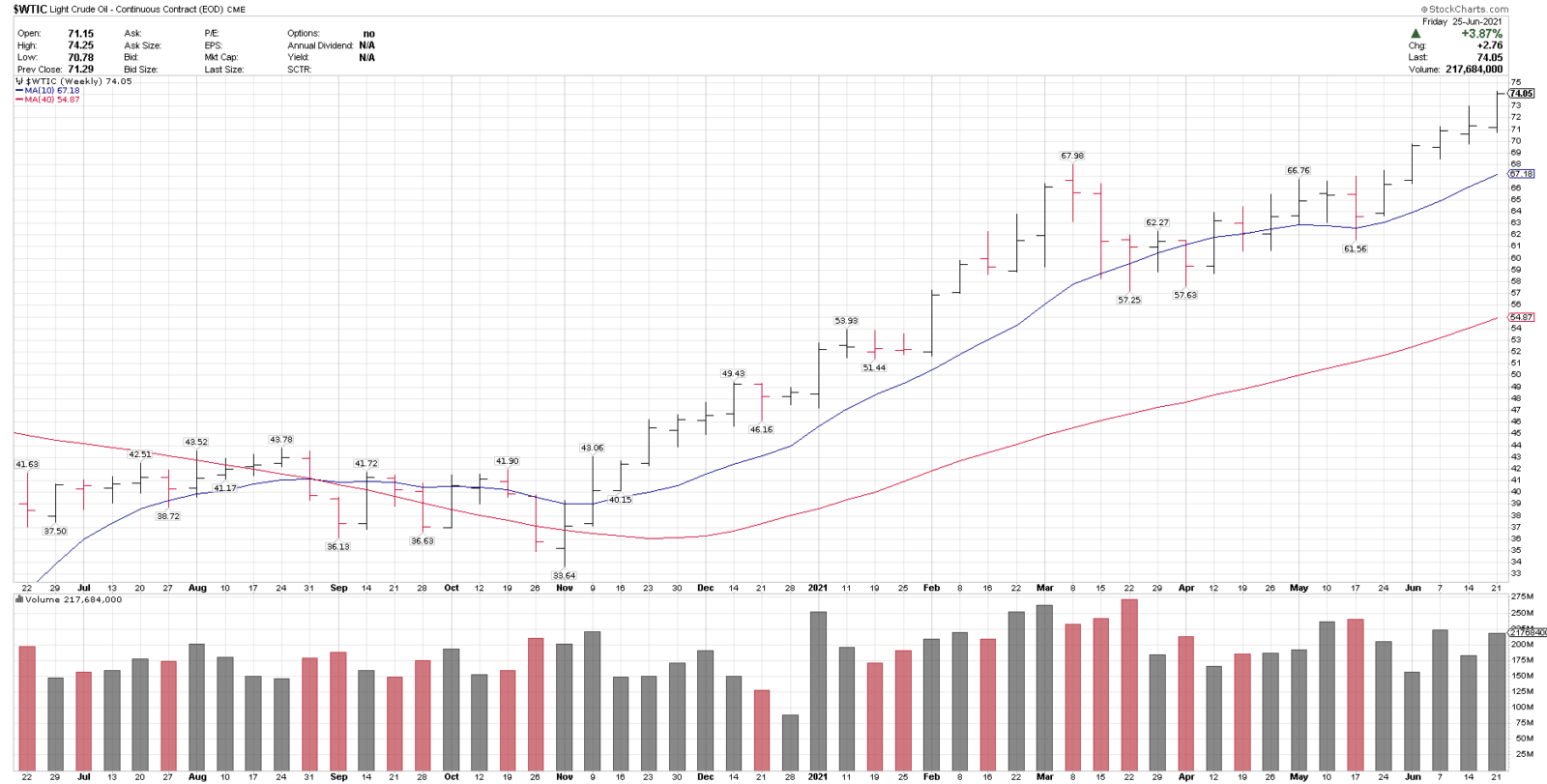

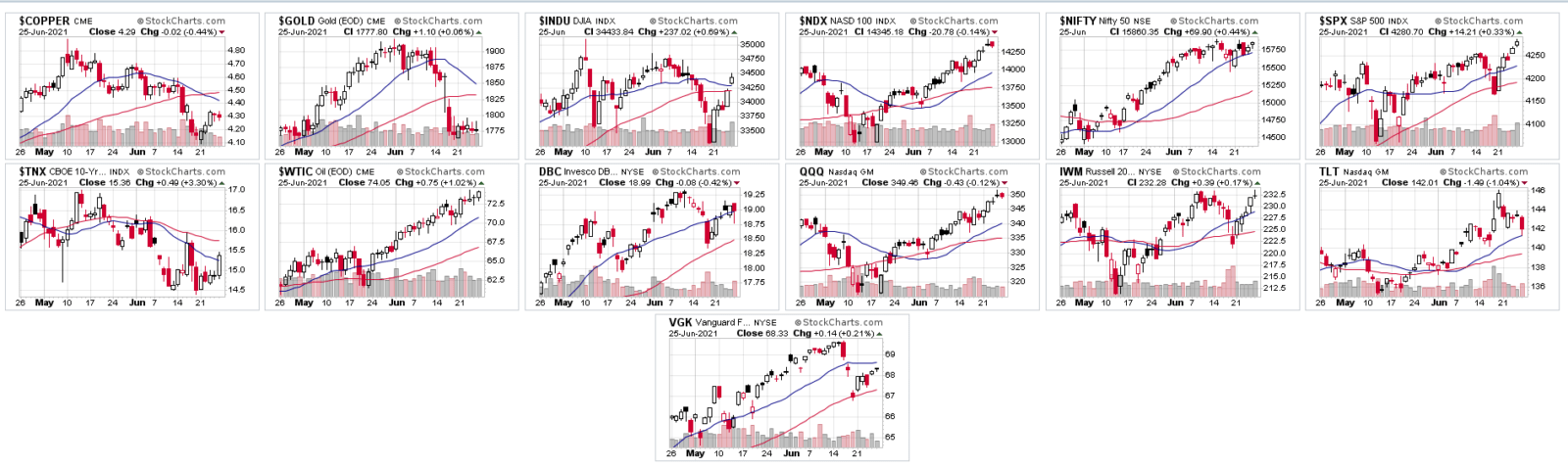

- WTI crude oil (74.05) made another weekly closing high, the highest since October 2018.

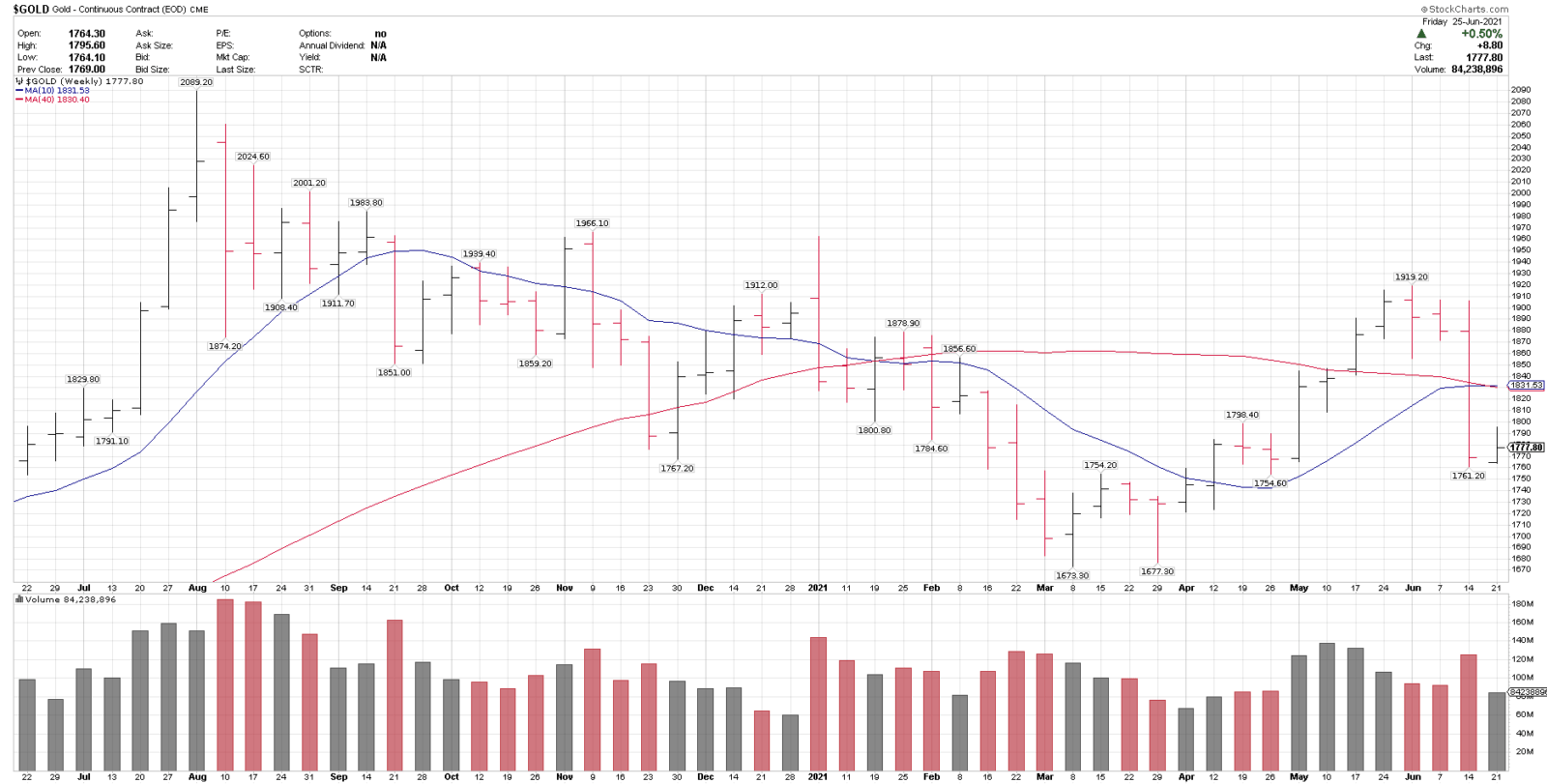

- Copper (4.29) held above the key $4.00 level (4.29) , Gold (1777.80) closed below $1800 for the second consecutive week.

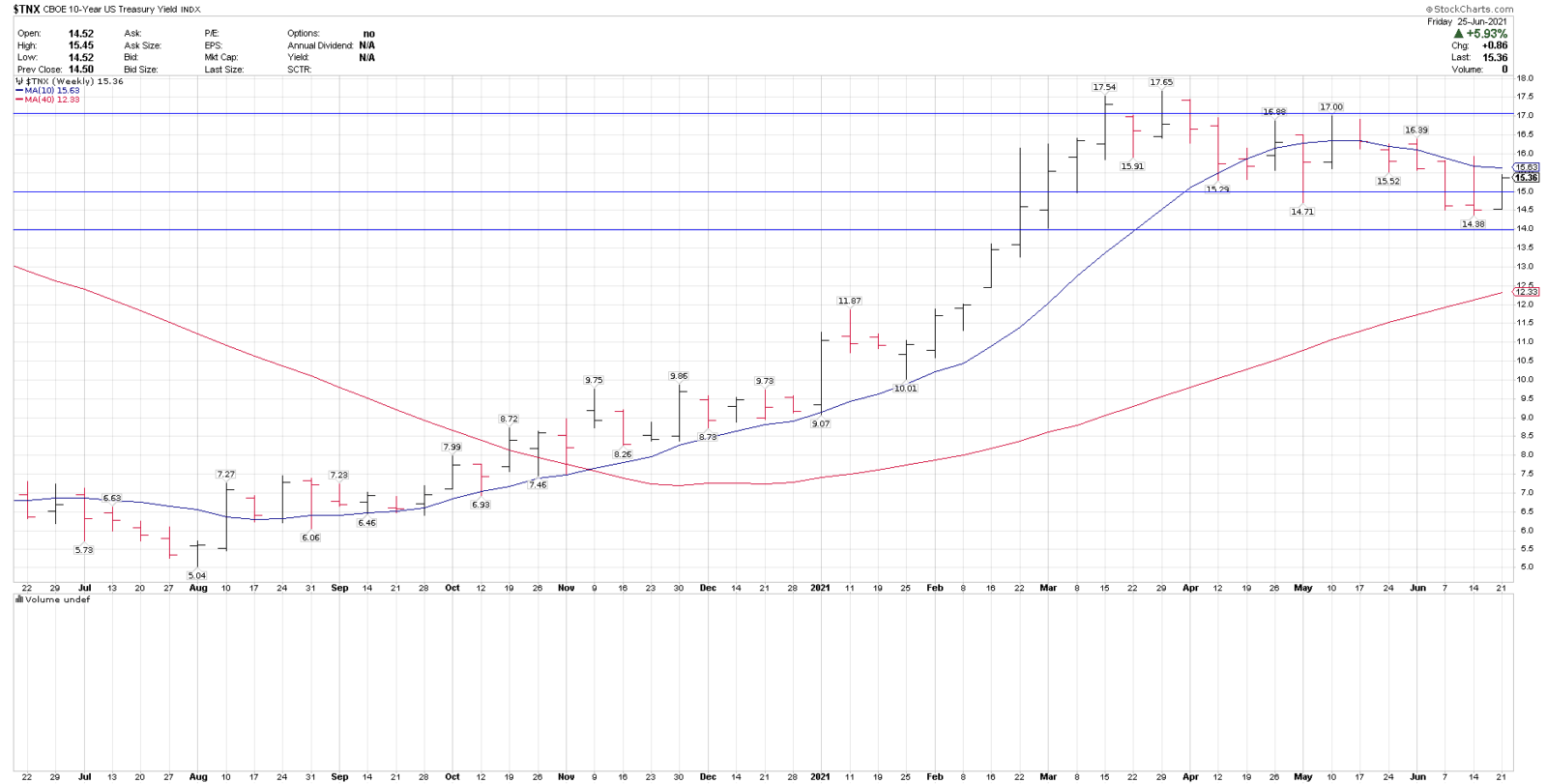

- 10-year UST yields (1.536) continue to hold over the 1.40 longer-term support level.

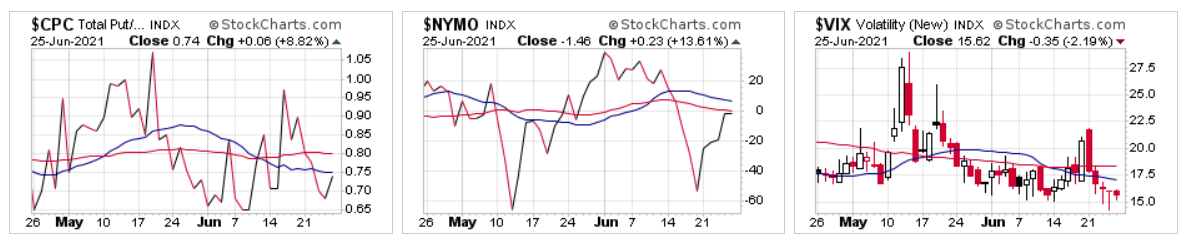

- VIX (15.62) put in the lowest weekly close since Feb. 2020.

————————— - Core ETFs top performers for the week: XOP, XRT, KRE, XLF, IWM

- Core ETFs top performers year-to-date: XOP, XRT, KRE, DBC, XME

- Core ETFs that made new weekly closing highs: QQQ, SPY, XLC, XLK, XLV, XOP, XRT

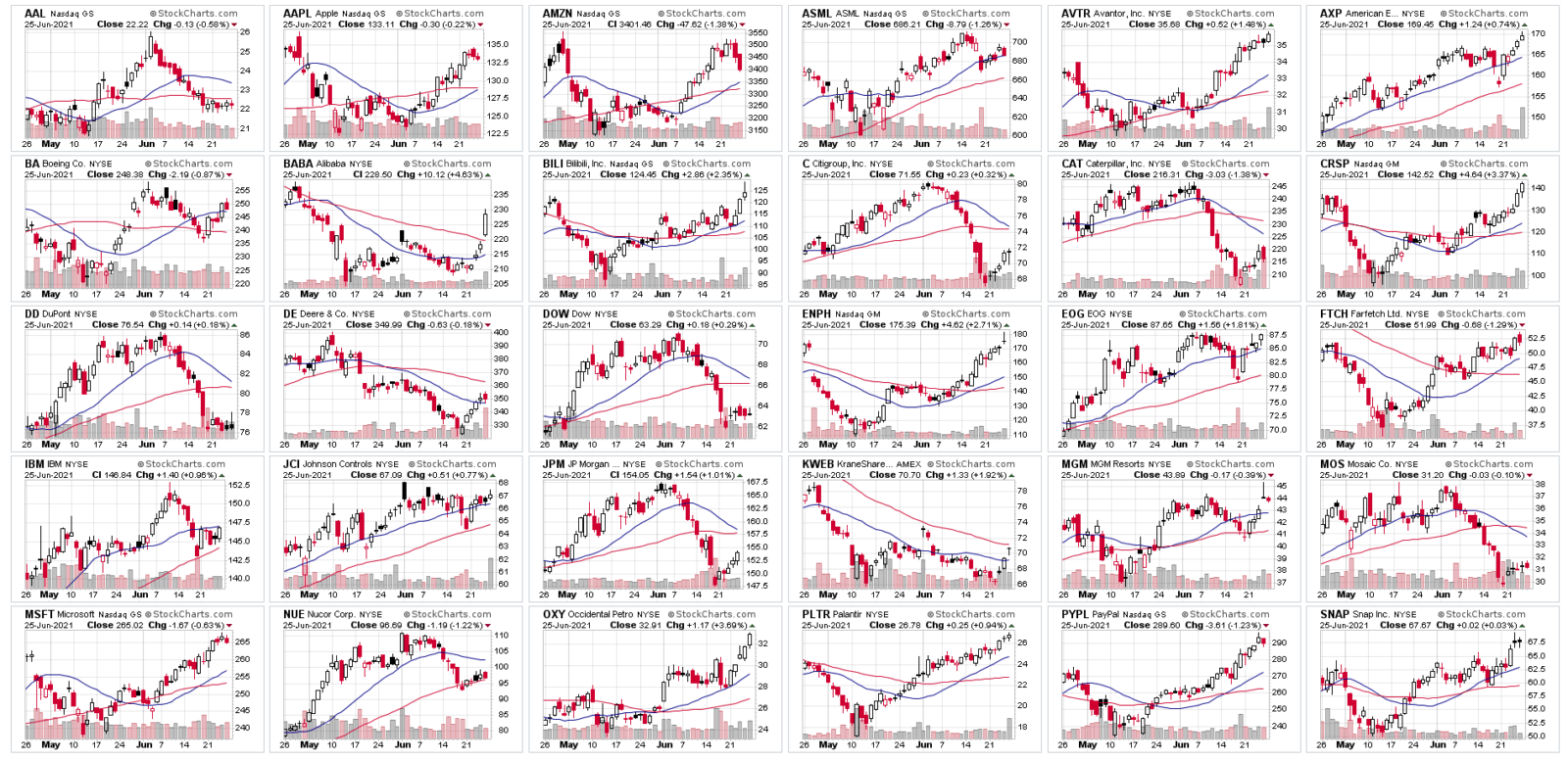

CORE MARKETS PERFORMANCE – LAST 30 DAYS

SPX SECTORS PERFORMANCE – LAST 30 DAYS

MARKET INTERNALS

*The ETF performance data below will be listed in last week/last 30 days/ytd percentage gain (%) format.

6/27/21

TOP RANKED FOCUS INDUSTRY GROUPS OVERVIEW

Note: A list of top ranked stocks by sector can be seen here: https://bluechipdaily.com/members/this-weeks-best-ideas-list/

1. Technology

- Nasdaq 100 ETF (QQQ), 1.99/4.59/11.39

- Semis (SMH), 2.68/3.38/16.08

- Cloud (CLOU), 2.07/9.02/2.65

- NDX and QQQ made new all time daily and weekly closing highs.

- Our view remains that if bond yields stay in check, and under 1.65 to 1.70, that should bode well for tech and growth stocks, which continues to play out.

- Growth stocks continue to outperform, especially in cloud software.

- Semis have been relative under-performers, as the market has shifted into more higher growth stocks. NVDA has had multiple breakouts, and AMD, AMAT and ASML are also focus charts.

- AMD closed at an 18-week high and is over the 40-week MA.

- As noted over the last few weeks, there continues to be improving trend momentum in tech with many 200-sma reclaims and/or bullish 20-50 sma crosses.

- Over last few 6 weeks or so, the market has shifted from lower valuation tech (STX, HPQ, DELL) into higher beta, higher growth sectors.

- Select BCD focus stocks: AMAT, AMD, ASML, NVDA/CRM, CRWD, FTNT, MSFT, NET, SE, SHOP, SQ/PYPL/ENPH.

2. Communication Services

- XLC, 2.63/2.41/19.52

- FB and GOOGL remain our top two ideas in this sector, but the group overall has been improving as growth stocks have resumed leadership.

- SNAP, ROKU, PINS, TWLO, ZM, BILI, IPG, NWS are other focus charts in this sector.

- As noted last week, the China internet sector has been lagging (BABA, BIDU, JD, PDD, VIPS), but improved last week, with KWEB +4.32% on the week.

- BABA was up on high volume, but has work to do, under the 200-sma, 200 is key support. BIDU reclaimed the 50-sma for the first time since March 2021.

- VIAC may offer a longer term recovery idea, and closed at an 11-week high, but should be consider higher volatility here as well. 37.50 is key long-term support.

- Select BCD Focus Stocks: FB, GOOGL, PINS, ROKU, SNAP, BIDU, BILI, IPG, TWLO, VIAC, ZG, ZM.

3. Energy

- XOP, 9.30/13.78/70.51

- WTI continued it’s new high streak, to close at 74.05, and the highest level since October 2018.

- WTI continues to hold in it’s strong uptrend and has broken away from other commodity groups that have had sharp pullbacks.

- Crude oil has it’s own supply/demand and pricing dynamics and continues to trend higher here, although it has sharp pullbacks along the way.

- Select BCD focus stocks: EOG, MRO, XOM, FANG, OXY, BP, COP, CVX, DVN, HAL, HES, LNG, SLB.

4. Financials

- XLF, 4.83/-1.49/25.27

- KRE, 6.25/-2.70/30.20

- Large cap financials had a nice recovery week, along with DIA.

- This group will likely continue to trade with bond yields (TNX), which are near the lower end of their range and over 1.40.

- A list of core tracking financials that held recent MA tests:

Held > the 50-sma: AXP, BLK, KKR, TD.

Held > the 100-sma: AIG, ALLY, BAC, COF, GS, MS, WFC

Held over and did not test the 50-sma: BMO, BX, CG, MCO, RY. - Select BCD focus stocks: BAC, C, JPM, WFC/AXP, COF/BMO, RY, TD/BLK, BX, KKR, MCO

5. Healthcare

- XLV, 1.58/1.87/10.81

- IBB, 2.75/8.33/7.68

- ARKG, 3.99/11.44/-3.41

- Healthcare has been a less volatile sector and XLV made new all-time highs last week.

- There has been alot of separation in the group, and not any general sector breakouts.

- Biotech is starting to improve and REGN is trending above the 200-sma.

- The more speculative industries in genomics and biotechnology have been more volatile and should be considered higher risk, but have been improving with growth stocks.

- Select BCD focus stocks: ABBV, AZN, GSK, GILD, LLY, PFE, REGN/ HCA,UNH/A, ALGN, BSX, CVS, DHR, ILMN, MDT

6. Basic Materials

- This is one of the most diversified sectors, but can also be more volatile than average.

- XME, 4.14/-4.48/28.65

- XLB, 1.72/-5.23/13.45

- We continue to believe that there is a commodity upcycle underway, and this sector could be a top performer over the next 3-6+ months if so, with sharp pullbacks along the way.

- This sector should benefit from any potential major increased infrastructure spending, but we want to see this actually show up on the charts, in the form of higher prices and new uptrends.

- Agriculture, chemicals, copper, fertilizer, lithium, metals, mining, potash and steel are top focus groups.

- Select BCD Focus stocks: FCX, MT, CLF, NUE, STLD, TECK, VALE /ALB, CF, CX, MOS, NTR/ DOW, DD, IP/FNV, NEM, WPM.

7. Consumer Discretionary (Autos, Home Construction, Retail, Travel, etc.)

- Focus Consumer Discretionary industries include: Apparel, auto manufacturers, footwear, furnishings, home improvement retail, online retail (e-commerce), residential construction, & specialty retail.

- This is maybe the most diversified sector, with exposure to autos, general retail, online retail and travel, among other industries.

- There were a few leaders that started to weaken, but have recovered, such as LB.

- Select BCD focus stocks: CZR, EXPE, MGM/ F, GM/ DHI, LEN, PHM, TOL/ GPS, LB, SBUX, TGT

8. Industrials

- XLI, 2.75/-1.30/15.58

- Core industries in this sector include: Aerospace & Defense, Airlines, Building Products & Equipment, Farm & Heavy Construction Machinery, Freight & Logistics, Railroads, Specialty Industrial Machinery and Trucking, among others.

- The industrials group overall could benefit from increased infrastructure spending, but coming into this week, has very few qualifying charts in uptrends.

- CARR, GNRC, JCI and OTIS are standout uptrends.

- Select BCD focus stocks: BA, GNRC, GD, GE, OTIS, RTX/FDX, UPS/ CARR, JCI, TT/AAL, UAL.

9. Renewable Energy

- The renewable energy sector (clean energy) is our top ranked potential reward vs risk group coming into this week.

- This is a very volatile sector, which had drawdowns from -35% to -75% in the recent growth stock sell off.

- This group includes solar, renewable energy, EV’s and other related industries.

- There have been multiple constructive price and trend developments over the last few weeks, and solar/clean energy has been on the High Beta list for the last two weeks.

- ENPH is the large cap leader. QCLN and TAN offer ETF exposure to the group.

10. Real Estate (REITs)

WEEKLY MACRO CHARTS

SPX

SPX is in a longer-term technical uptrend and made a new all-time high and weekly closing highs last week. This market is constructive over 4050 & 3850.

BCD Trend Rating: LT Uptrend, accumulate.

NDX

NDX made a new all-time high and weekly closing high. 13400 & 12600 are key support levels.

BCD Trend Rating: LT Uptrend, accumulate.

TNX

The near term trend is down in TNX, and up in UST’s. 1.40 is major longer-term support.

BCD LT Trend Rating: Neutral, consolidation in yields. 1.40 – 1.50% are key levels on any pullbacks.

WTI CRUDE OIL

Crude oil is in a longer-term uptrend and made the highest weekly close again since 10/2018.

BCD LT Trend Rating: Uptrend, accumulate.

GOLD

Gold closed below the 40-week sma and below 1800 for the second consecutive week.

BCD LT Trend Rating: Neutral. 1675 is a major support level.

This Week’s Best Ideas List Page: https://bluechipdaily.com/members/this-weeks-best-ideas-list/

THIS WEEK’S ETF BEST IDEAS LIST:

- We screen for ETFs that we believe can out-perform based on their current trend.

- We always expect market and or/position volatility.

- Our standard trend following stop level is currently at 15% for new positions.

QQQ, SMH, XLC, XLF, XLV, XOP

THIS WEEK’S BEST IDEAS TOP 25 STOCKS LIST:

- We screen for stocks that we believe can out-perform based on their current trend.

- We always expect market and or/position volatility.

- Our standard trend following stop level is currently at 15% for new positions.

- EARNINGS: Please check earning reporting dates for any names of interest.

- All data should be independently verified.

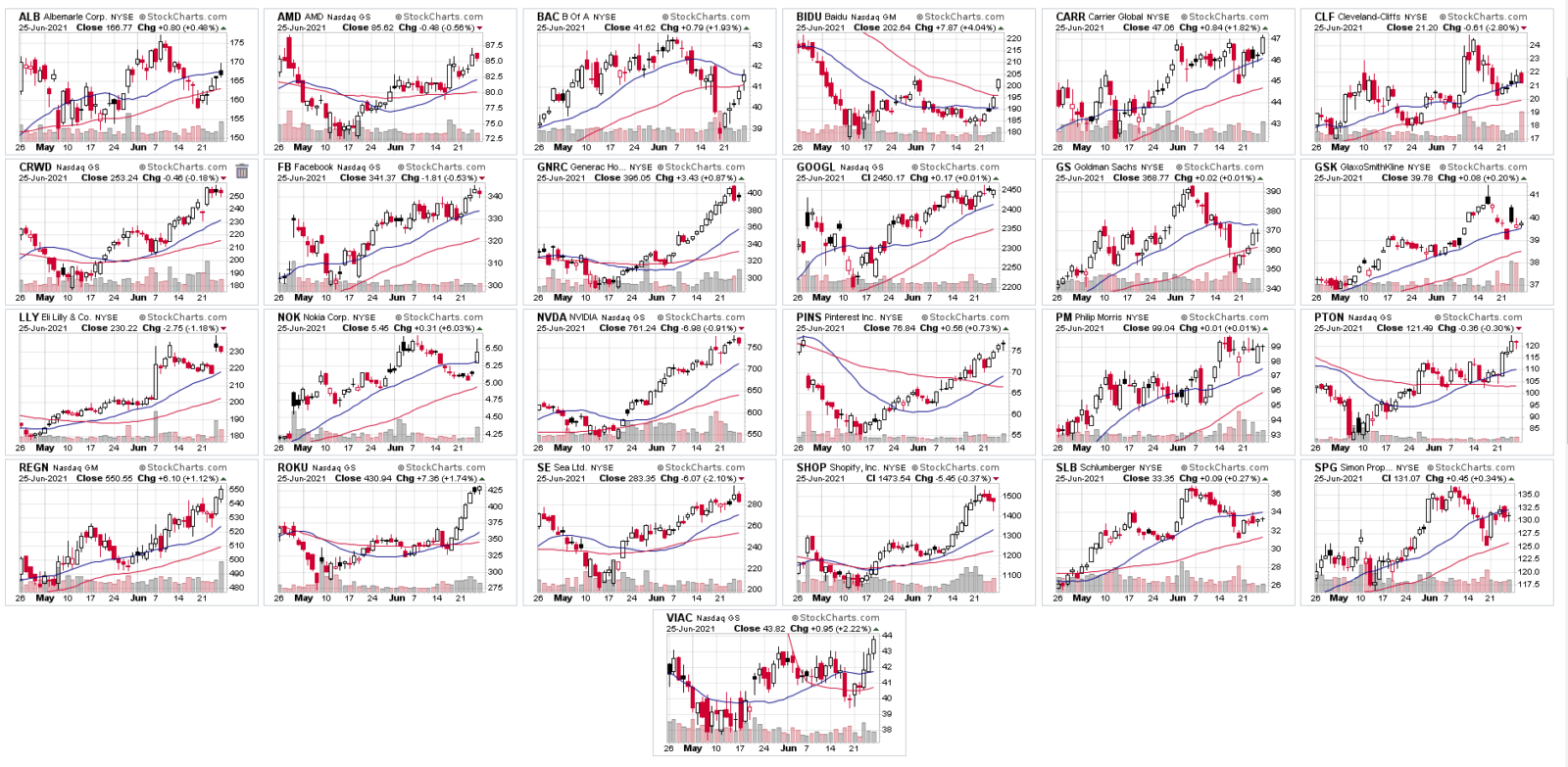

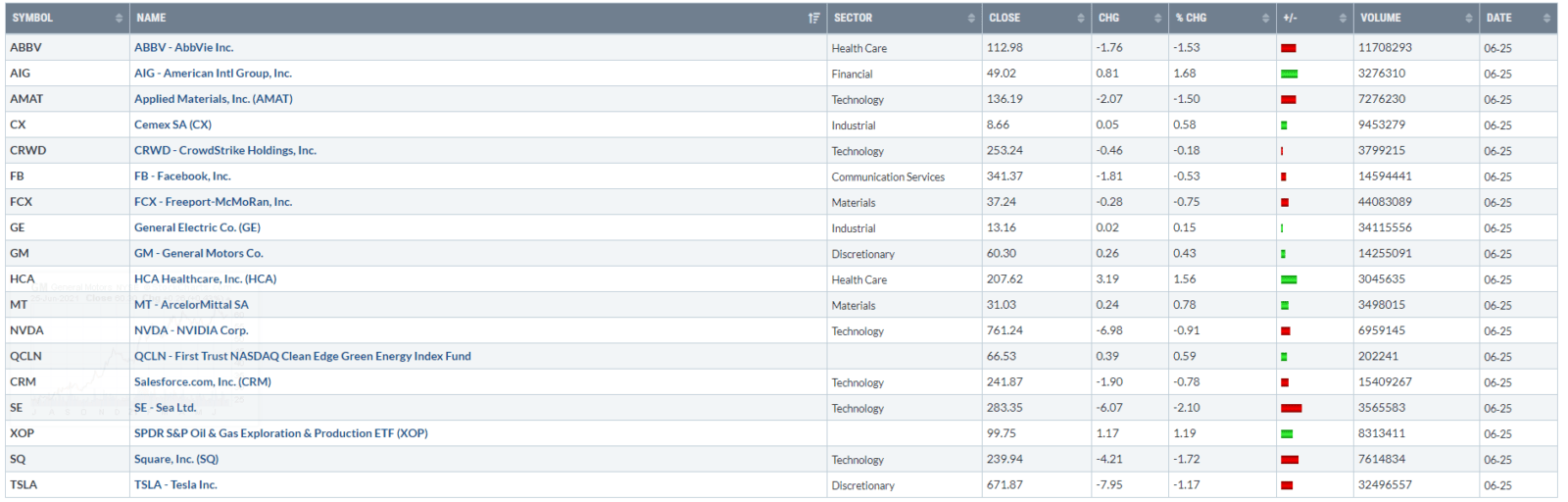

ALB, AMD, BAC, BIDU, CARR, CLF, CRWD, FB, GNRC, GOOGL, GS, GSK, LLY, NOK, NVDA, PINS, PM, PTON, REGN, ROKU, SE, SHOP, SLB, SPG, VIAC

MAJOR MARKETS OVERVIEW: (Our top down overview, and date of first post.)

- We continue to believe that there is a major cyclical and economic recovery underway, that travel and consumer spending will be higher than many expect, and that a commodity/infrastructure up-cycle is underway as well. (8/2020)

- We believe that “growth at a reasonable price” (GARP) will be a key factor in Q2, and select tech and communication services stocks fit into this category. (3/2021)

- The recent breakouts in mega cap leaders such as AMZN, FB, GOOGL, MSFT and NVDA, looks to be the start of a new uptrend higher, although there will be pullbacks along the way. (4/2021)

- We think the best approach here is a combination of high quality growth & cyclicals names, plus some exposure to lower volatility sectors, (healthcare, select staples) all in uptrends, slightly higher cash and wider stops based on market volatility. (5/2021)

- ARKK, QQQ and many growth stocks reached key oversold levels on daily charts: (5/2021)

https://twitter.com/BlueChipPremium/status/1393245045910822914

https://twitter.com/BlueChipPremium/status/1393179499471200257 - We believe that 10-year US Treasury bond yields (TNX) will remain a key factor, and high growth stocks, tech and precious metals are most affected, in either direction. (6/2021)

- As long as bond yields don’t breakout to the upside and economic reports come in moderate (good, but not great), this should bode well for equities. (6/2021)

WEEKLY SECTOR SUMMARY & PREVIEW

- Growth sectors continue to outperform, with NDX, QQQ, and XLK making new weekly closing highs.

- QQQ put in the recent low on 5/12 and TNX peaked at 1.70 on 5/13.

- Noted last week: “NYMO (NYSE McLellan Oscillator) closed at -53.67, and near oversold levels that often mark near term market lows/reversals.” This led to new highs in SPX and NDX, and the best week in SPX since February 2021.

- Current relative strength leaders are in cloud, biotech, Nasdaq 100, genomics and solar – higher growth groups.

- Energy and WTI crude oil have continued to show relative strength, with both making closing highs on Friday.

- Potential beneficiaries of proposed major increased infrastructure spending include basic materials and industrials, though this follow through remains to be seen.

- Financials pulled back with cyclicals recently, but the positive Bank Stress Test results could prove to be a needed catalyst, which could allow for increased dividends and share buybacks.

- Clean energy (QCLN, TAN) is our top ranked potential reward vs risk sector here. It is also one of the more volatile groups.

- China Internet may be starting a recovery attempt.

SUMMARY

- I’m currently at 29% cash, which is much higher than average, due to many booked gains in cyclicals over the last 6 weeks, and the close out of a few lagging positions. https://bluechipdaily.com/open-positions-ideas/

- I plan to reallocate some of it this week.

- Growth sectors continue to outperform, and many weekly charts have broken out and turned up in their trends.

- The longer-term cyclical recovery is still intact, though another strong week of recovery would help. My key focus here remains charts that are in uptrends over the 50-sma.

- Defensive sectors such as staples and defensive healthcare stocks have stalled for now.

- Markets are still very focused on FOMC news and the constant flow of economic reports and data, as the markets try to gauge where we are in the recovery cycle and at what stage the Fed needs to step in or not.

- As long as economic data stays moderate, good but not great, and bond yields don’t breakout to the upside, this should be favorable for stocks overall.

- For now, SPX remains in a steady uptrend and NDX broke out to new highs.

- The cyclical charts are at various stages of recovery/uptrends, so we will continue to maintain a chart specific focus on leading stocks and the sectors as well.

- Markets and stocks don’t always go straight up, so pullbacks and consolidation along the way are part of the process, but the overall longer-term charts are set up well here.

Have a great week,

Larry Tentarelli

Publisher

OPEN POSITIONS:

CORE MARKETS:

CORE MARKETS:

ADDITIONAL CHARTS COVERED IN TODAY’S VIDEO: