WEEKLY TREND REPORT

SUNDAY, MAY 23, 2021

WEEKLY MARKETS RECAP

- There were no new highs in the major U. S. indices last week.

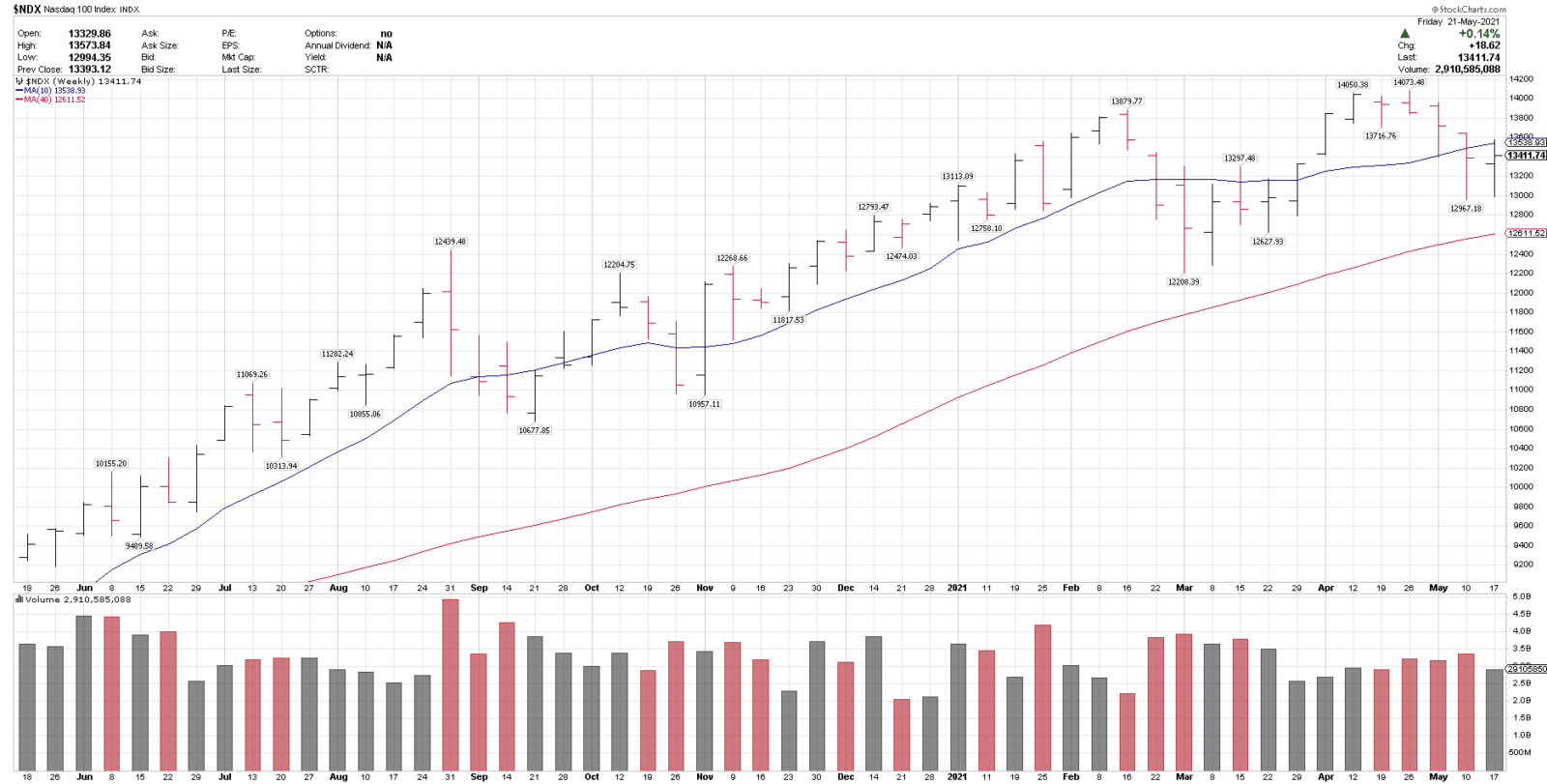

- NDX and QQQ closed higher on the week for the first week in five.

- Europe (VGK) made a new all-time high and weekly closing high.

- India (NIFTY) made a new all-time weekly closing high.

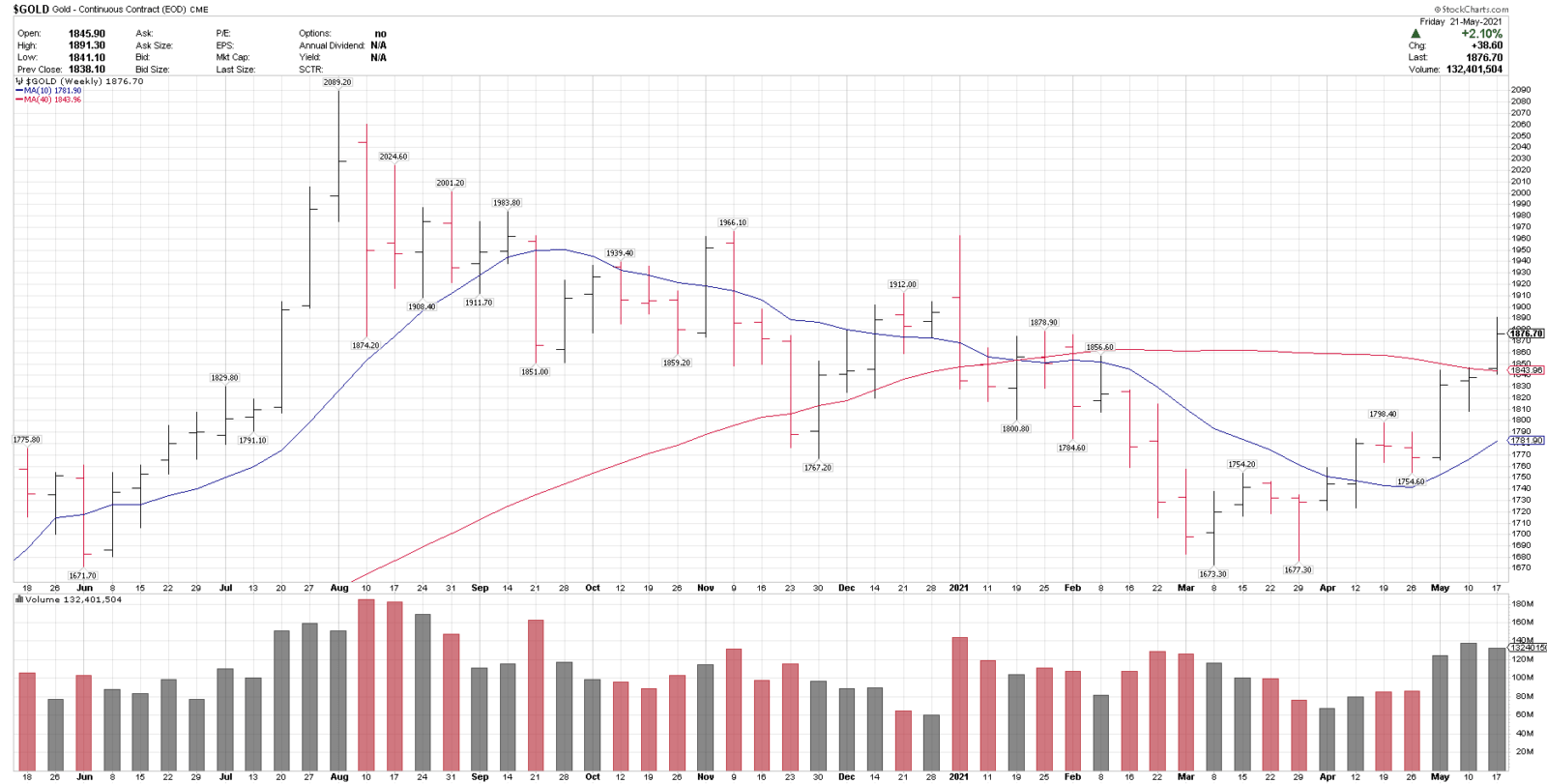

- Gold had it’s first close over the 40-week MA since January 2021 and had the second weekly close over the key 1800 level.

- GDX had the third consecutive weekly close over the 40-week MA, on rising volume.

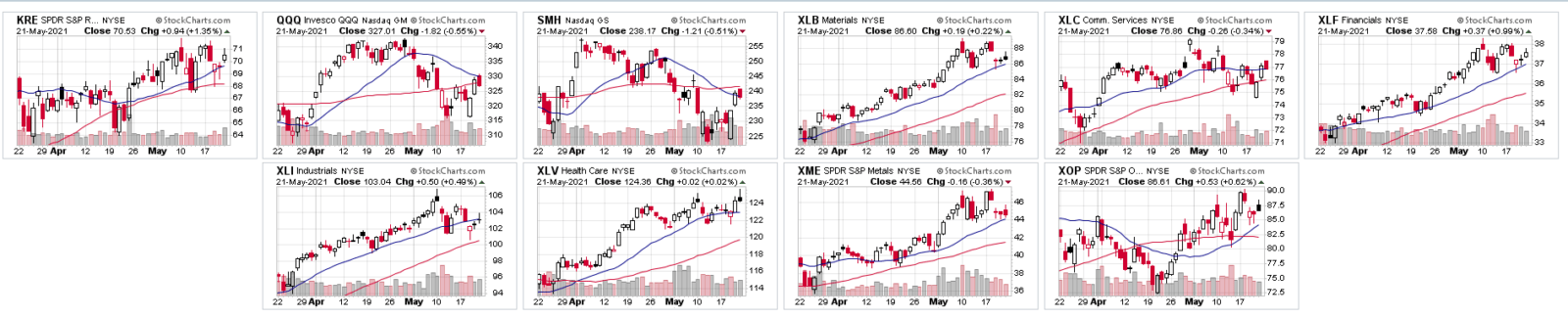

————————— - Core ETFs top performers for the week: TAN, QCLN, GDX, KWEB, CLOU

- Core ETFs top performers year-to-date: XOP, XRT, KRE, XME, XLF

- Core ETFs that made new weekly closing highs: INDA, VGK, XLP, XLV

CORE MARKETS PERFORMANCE – YTD

SPX SECTORS PERFORMANCE – YTD

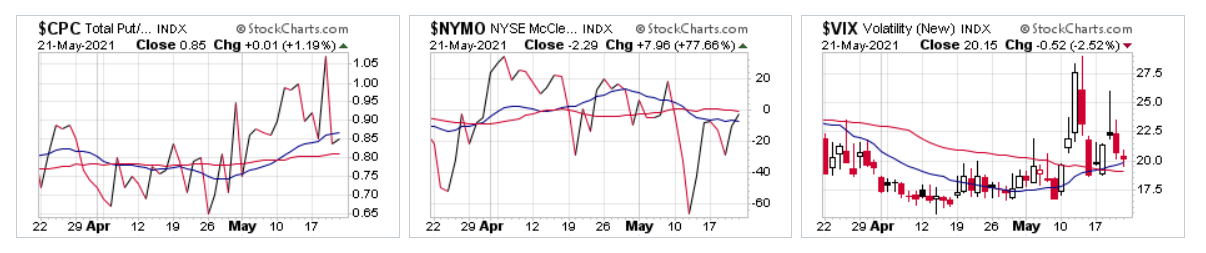

MARKET INTERNALS

5/23/21

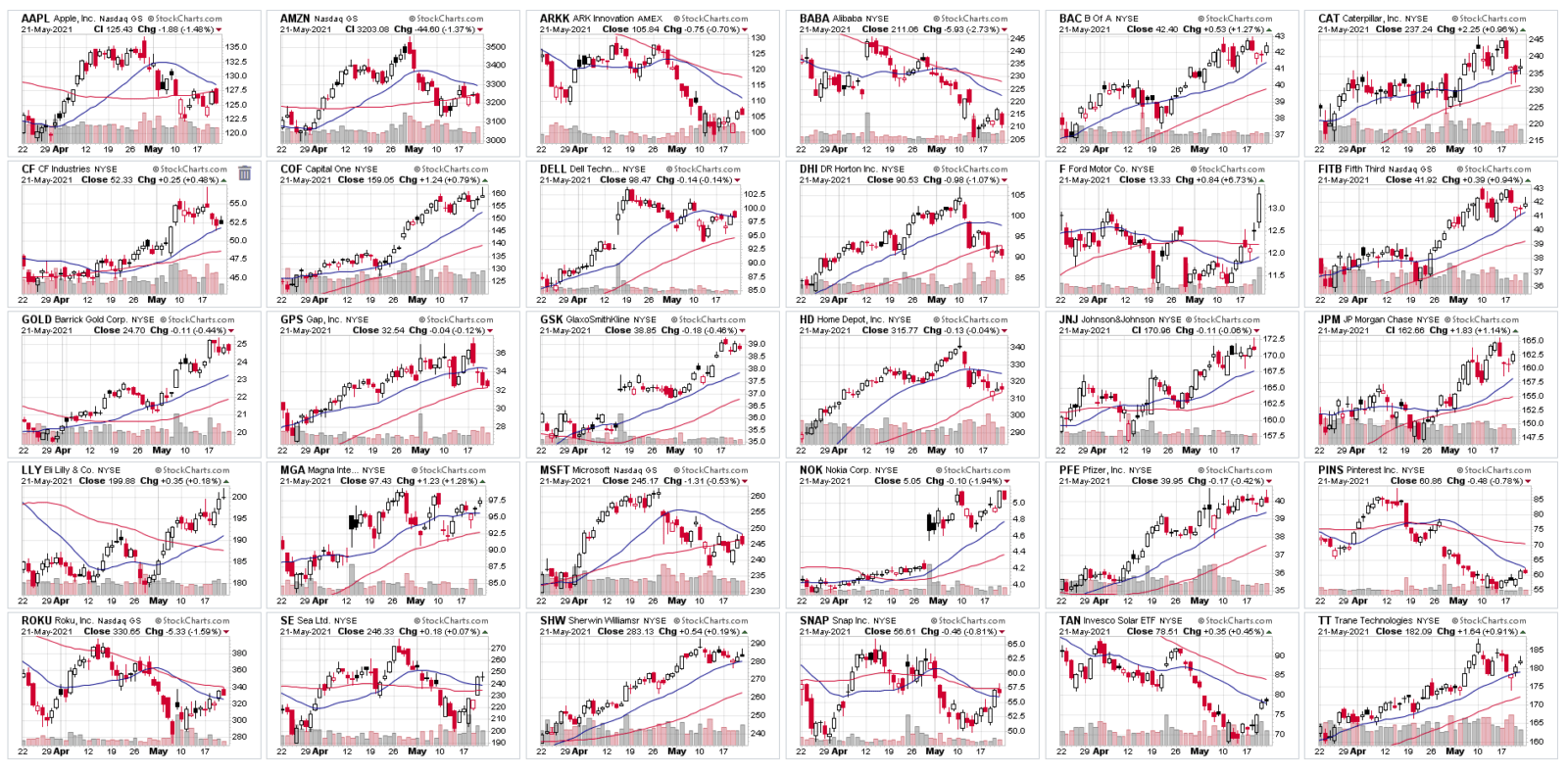

TOP RANKED FOCUS INDUSTRY GROUPS OVERVIEW

Note: A list of top ranked stocks by sector can be seen here: https://bluechipdaily.com/members/this-weeks-best-ideas-list/

1. Financials

- XLF, -0.79% week, +27.48% ytd.

- KRE, -0.94% week, +35.77% ytd.

- Large cap financials remain our top ranked sector again this week, based on their current charts, lower valuation, higher dividends and position in the cycle.

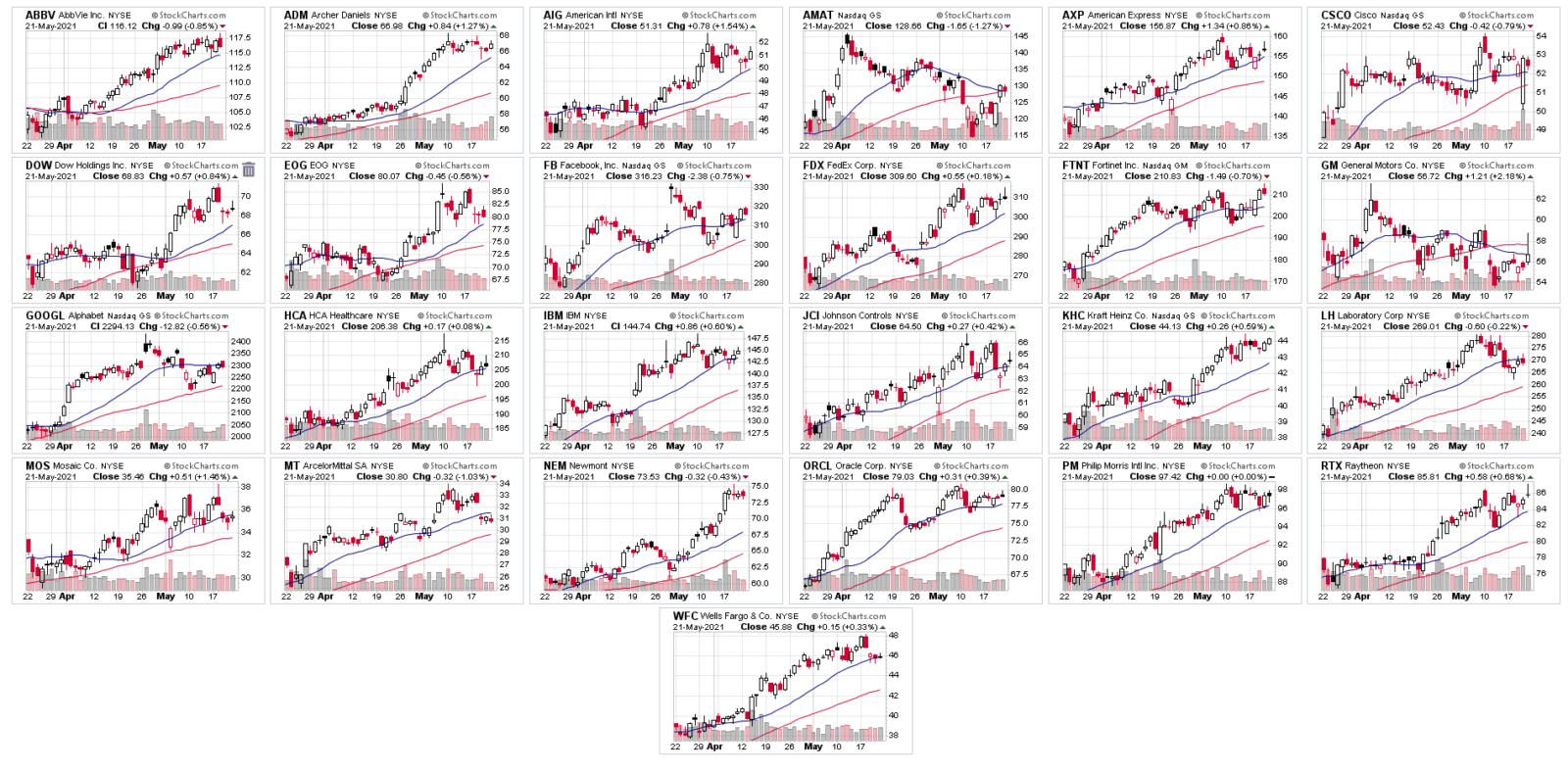

- BAC broke out to a new all-time high.

- C made a 12-year weekly closing high.

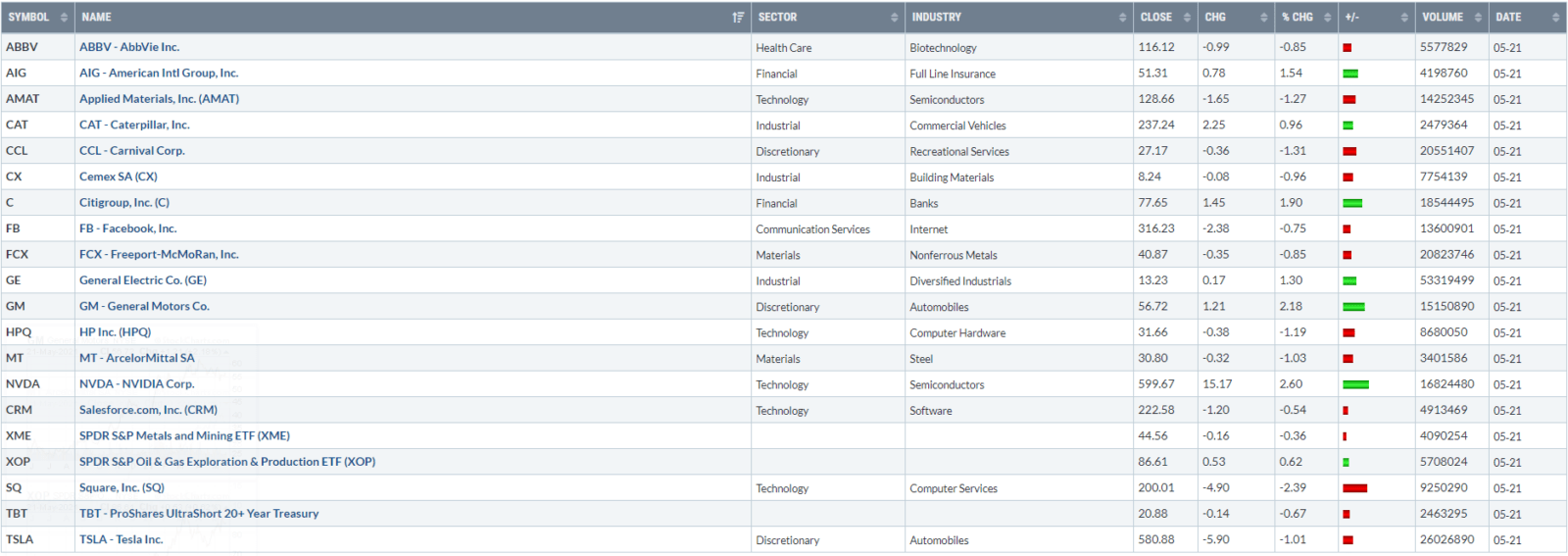

- Select BDC focus stocks: AIG, ALLY, AXP, BAC, BX, C, COF, FITB, GS, JPM, KKR, MS, SCHW, WFC.

2. Basic Materials

- This is one of the most diversified sectors, but can also be more volatile than average.

- XME -1.18% week, +33.25% ytd.

- XLB -1.49% week, +19.63% ytd.

- GDX +3.83% week, +9.08% ytd.

- We continue to believe that there is a commodity upcycle underway, and this sector could be a top performer over the next 3-6+ months if so, with sharp pullbacks along the way.

- This sector could also benefit from any increased infrastructure spending.

- Agriculture, chemicals, copper, fertilizer, lithium, metals, mining, potash and steel are top focus groups.

- XME is our top ranked potential upside group in this sector, XLB is lower volatility and GDX is a high potential return/risk idea.

- Select BCD focus stocks: CF, CX, DOW, FCX, FNV, GOLD, MLM, MOS, MT, NEM, NTR, NUE, SHW, STLD, TECK, VALE, VMC, WPM.

3. Industrials

- XLI, -1.61%week, +16.36%ytd.

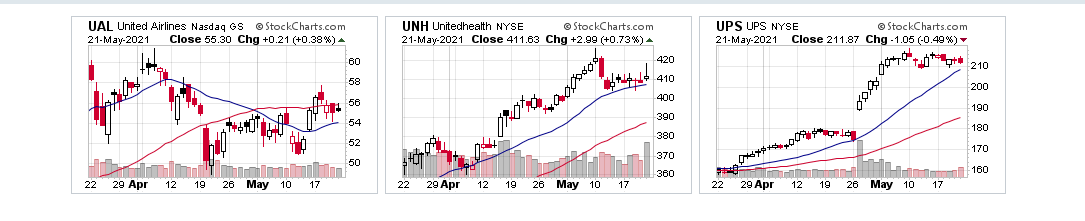

- Core industries in this sector include: Aerospace & Defense, Airlines, Building Products & Equipment, Farm & Heavy Construction Machinery, Freight & Logistics, Railroads, Specialty Industrial Machinery and Trucking, among others.

- Overall, the single stock charts in the industrial sector are still among the strongest uptrends on our screen.

- Building materials, aerospace/defense & delivery service charts are set up well.

- We think that airlines also offer longer-term upside potential.

- FDX, JCI, RTX and TT uptrends standout here, among others.

- Select BCD focus stocks: CARR, CAT, CSX, DE, FDX, GD, GE, HON, JCI, LUV, MMM, NSC, ODFL, OTIS, RTX, TT, UAL, UPS.

4. Technology

- Nasdaq 100 ETF (QQQ) +0.19% week, +4.23% ytd.

- SMH +2.07% week, +9.04% ytd.

- Our focus here remains higher quality, lower valuation tech (semis, telecom equipment, computer hardware), including AMAT, ASML, CSCO, DELL, GLW, HPQ, IBM, NOK, ORCL and STX.

- Also, higher quality GARP stocks such as FTNT, MSFT, and NVDA.

- CRWD and SHOP are higher beta cloud names back over the 50-sma, and may appear on this week’s High Beta List.

- We continue to think that semis have upside potential from here, after this recent pullback, and they led at +2.07% on the week.

- We think that alot of speculative money from late 2020, early 2021, has shifted into higher quality, profitable tech companies at more moderate valuations, and the charts confirm this.

- Our view is that the higher valuation cloud stocks (SNOW, U) could have sharp counter trend bounces, but are in longer term downtrends, at least for now.

- Select BCD focus stocks: AAPL, AMAT, ASML, CRM, CSCO, DELL, FTNT, GLW, HPQ, IBM, MSFT, NOK, ORCL, NVDA, SQ, STX.

5. Communication Services

- XLC: -0.30% week, +13.90% ytd.

- This sector has weakened slightly as prior performance leaders BIDU, BILI, PINS, ROKU, and SNAP have come under selling pressure over the last few weeks.

- FB and GOOGL are our top two ideas here and Se is a top ranked higher beta chart.

- VIAC may offer a longer term recovery idea, but should be consider higher volatility here as well.

- Select BDC focus stocks: FB, GOOGL, ATVI, IPG, NWS, OMC, SE.

- PINS, ROKU and SNAP are focus tracking stocks, are all below their 50-sma currently, and should be considered more volatile, higher return/risk charts.

6. Energy

- XOP +0.29%week, +48.05% ytd.

- XLE -2.49% week, +37.63% ytd.

- $72 is a key support level for XOP, which made a third consecutive close over the 10-week SMA.

- XOP and XLE are volatile sectors, but we like the reward vs risk from these levels.

- Select BCD focus stocks: EOG, FANG, OXY, BP, COP, CVX, DVN, HAL, HES, LNG, SLB, XOM.

7. Healthcare

- XLV +0.74% week, +9.63% ytd, and a new all-time weekly closing high.

- This sector continues to improve, and is outside of the traditional growth or value sectors.

- The sector overall has lower than average valuations, and above average dividends.

- The more speculative industries in genomics and biotechnology have been more volatile and should be considered higher risk.

- Select BCD focus stocks: A, ABBV, ABT, AZN, BSX, CI, CVS, GSK, HCA, JNJ, LH, LLY, MCK, MDT, PFE, UNH, WBA.

8. Gold & Gold Miners (higher volatility)

- GDX +3.83% week, +9.08% ytd.

- Gold and gold miners can be a higher volatility, high reward vs risk industry.

- Historically, Gold and Miners can trade inverse of TNX, but have been improving recently.

- GDX closed over the 40-week MA for the third week in a row, and was up on the week vs a down SPX.

- GDX Monthly chart from 4/8: https://twitter.com/BlueChipPremium/status/1380230860969017348

- Select BCD focus stocks: FNV, GFI, GOLD, NEM, WPM.

9. Consumer Discretionary (Home Construction, Retail & Travel)

- Focus Consumer Discretionary industries include: Apparel, auto manufacturers, footwear, furnishings, home improvement retail, online retail (e-commerce), residential construction, & specialty retail.

- The retail group pulled back last week, and may be starting to factor in the elimination of the unemployment assistance checks

- Home builders, building materials, and home improvement stores pulled back as well, with many homebuilders reporting that they can not get inventory in time. Both groups appear to be well positioned longer-term, though volatile near term.

- Auto parts is trending well, as it is a cyclical industry with low valuations, and new car supply is under pressure due to a semiconductor shortage.

- This sector is highly tied to a full reopening of the economy.

- Select BCD focus stocks: BURL, CCL, DHI, EXPE, F, GM, GPS, HD, LB, LEN, LOW, MGA, SBUX, TGT.

10. Consumer Defensive (new addition this week)

- In this sector we are much more focused on stock specific than the ETF, XLP.

- This sector offers many lower volatility uptrends, many with above average yields.

- ADM, BG, DEO, KHC, NWL, PM, TAP, TGT, TSN .

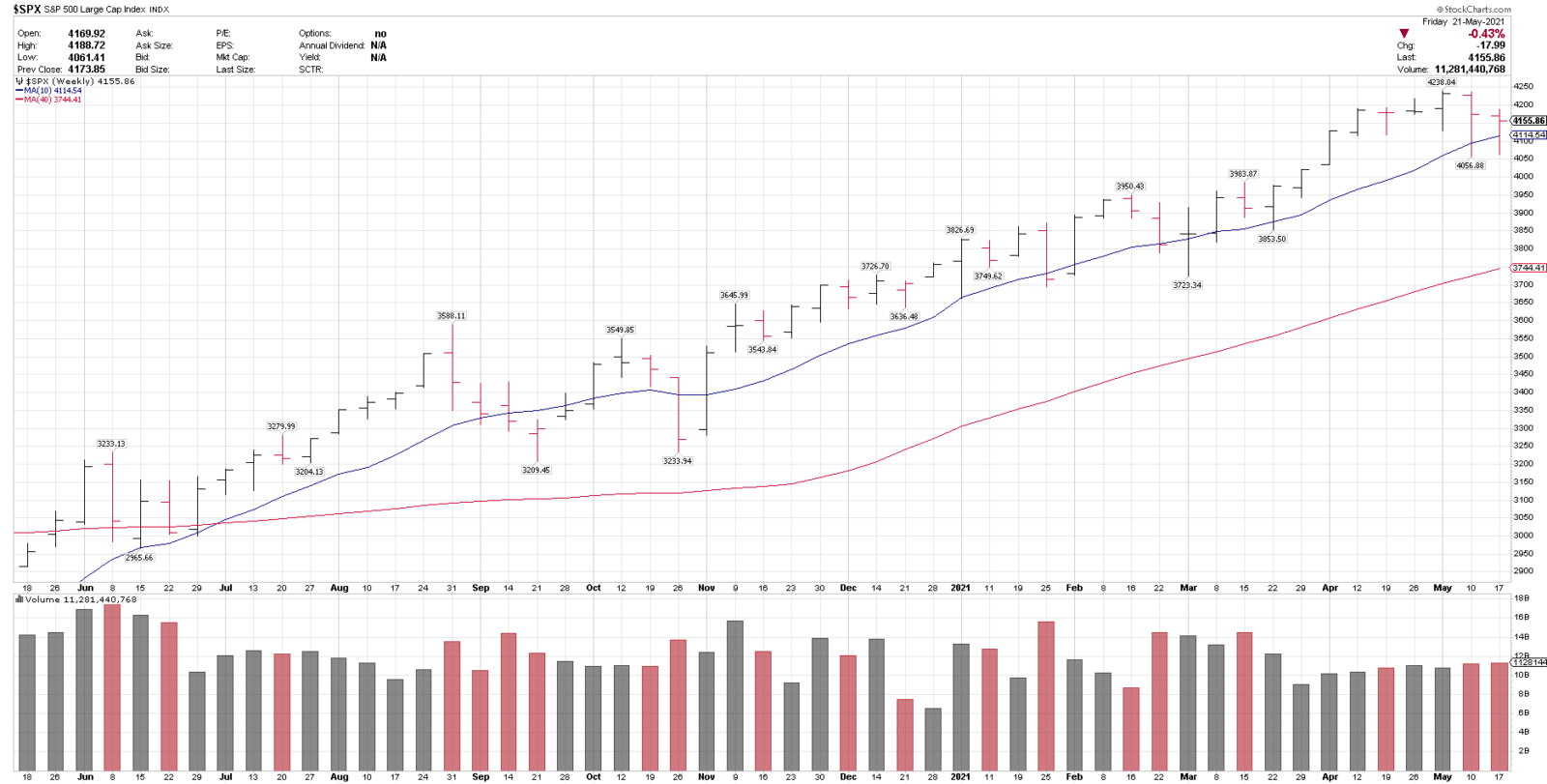

SPX WEEKLY

SPX is in a longer-term technical uptrend, and held the rising 10-week sma test for a second week. This market is constructive over 4050 & 3850.

BCD Trend Rating: LT Uptrend, accumulate.

NDX WEEKLY

NDX is consolidating in a longer term uptrend, and closed higher for the first week in 5. 13400 & 12600 are key support levels.

BCD Trend Rating: LT Uptrend, accumulate.

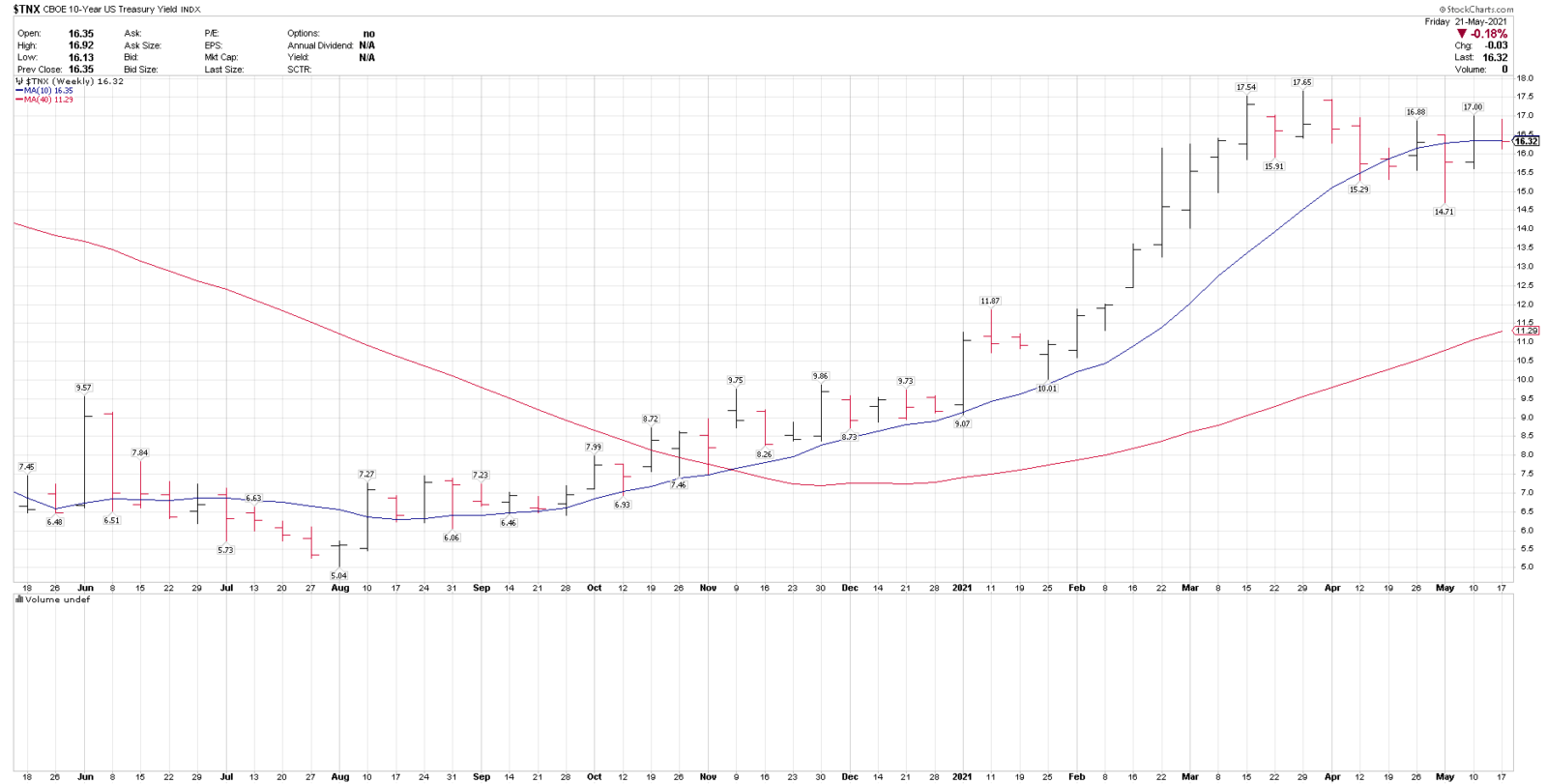

TNX WEEKLY

We continue to expect higher yields and lower bond prices in Q2 or Q3, but TNX is consolidating it’s recent 1.00 to 1.76 breakout move here. 1.00% is a key long-term support level and 1.40 to 1.50 in the near-term.

BCD LT Trend Rating: Uptrend in yields, which is currently consolidating. 1.40 – 1.50% are key levels on any further pullback.

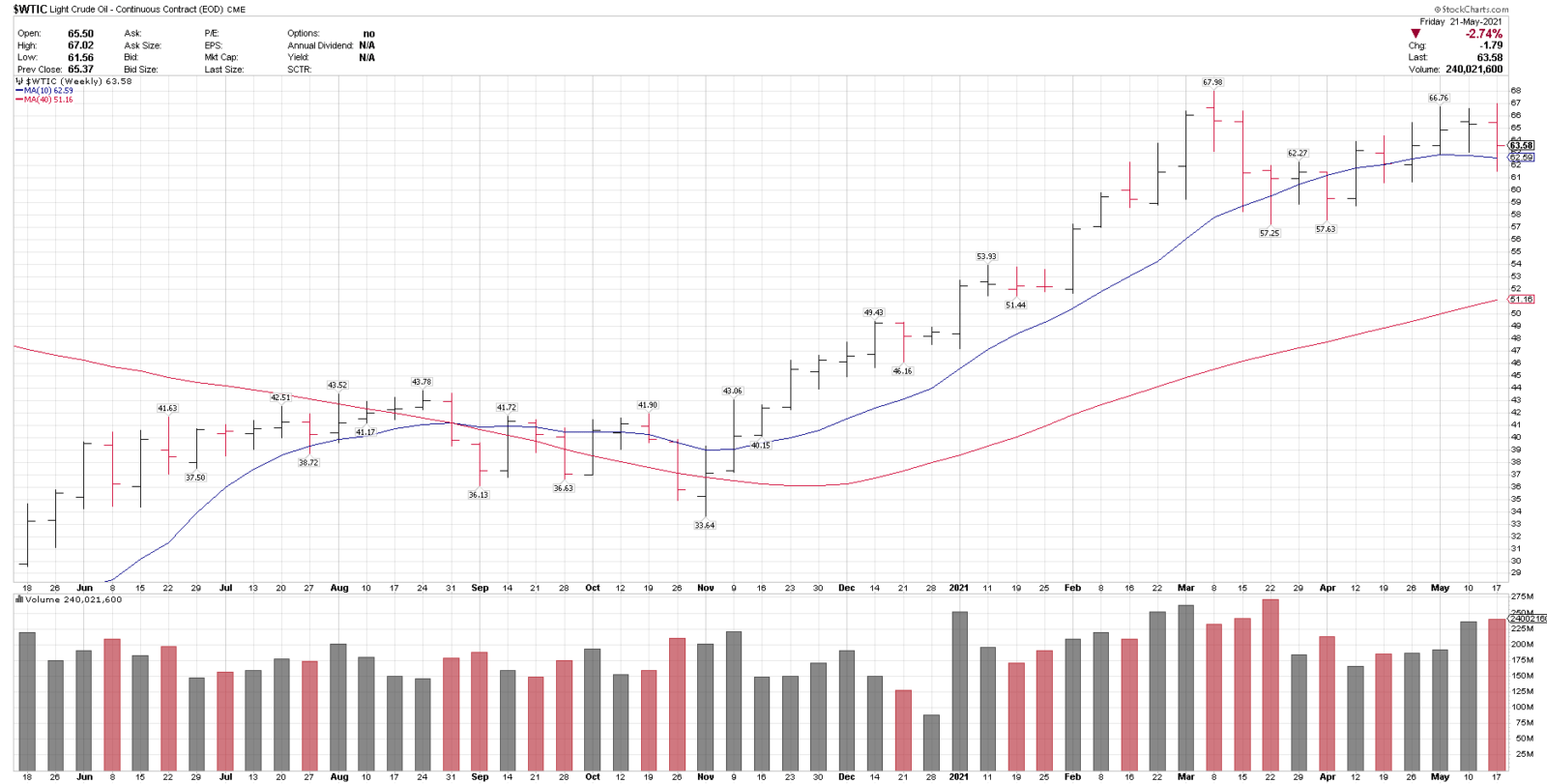

WTI CRUDE OIL WEEKLY

Crude oil is in a longer-term uptrend. $60, 57.50 and $50 are key technical breakout & support levels. This market stays constructive over $57.50. Over $68 could signal a breakout.

BCD LT Trend Rating: Accumulate.

GOLD WEEKLY

Gold made the first close over the 40-week MA since January 20212 and had it’s second weekly close over the key $1800 level.

BCD LT Trend Rating: Constructive over 1800. Near-term support is 1750 then 1675 is a major support level.

This Week’s Best Ideas List Page: https://bluechipdaily.com/members/this-weeks-best-ideas-list/

THIS WEEK’S ETF BEST IDEAS LIST:

- We screen for ETFs that we believe can out-perform based on their current trend.

- We always expect market and or/position volatility.

- Our standard trend following stop level is currently at 15% for new positions.

KRE, QQQ, SMH, XLB, XLC, XLF, XLI, XLV, XME, XOP

THIS WEEK’S BEST IDEAS TOP 25 STOCKS LIST:

- Ideas are considered actionable on the day they are posted.

- We screen for stocks that we believe can out-perform based on their current trend.

- We always expect market and or/position volatility.

- Our standard trend following stop level is currently at 15% for new positions.

- EARNINGS: Please check earning reporting dates for any names of interest.

- All data should be independently verified.

ABBV, ADM, AIG, AMAT, AXP, CSCO, DOW, EOG, FB, FDX, FTNT, GM, GOOGL, HCA, IBM, JCI, KHC, LH, MOS, MT, NEM, ORCL, PM, RTX, WFC

MAJOR MARKETS OVERVIEW: (Our top down overview, and date of first post.)

- We continue to believe that there is a major cyclical and economic recovery underway, that travel and consumer spending will be higher than many expect, and that a commodity/infrastructure up-cycle is underway as well. (8/2020)

- We also continue to believe, as we have since last August, that any pullbacks in the leading cyclicals should be buyable, as long as they trend above the rising 50-sma. (8/2020)

- We expect higher bond yields in the second half of 2021, if the reopening goes through without any major setbacks. (2/2021)

- In tech, we are staying focused on large cap tech stocks in uptrends at or near breakout levels, (semis, computer hardware, select software and IT services) and stocks that have reclaimed to 50-day MA. (3/2021)

- We believe that “growth at a reasonable price” (GARP) will be a key factor in Q2, and select tech and communication services stocks fit into this category. (3/2021)

- The recent breakouts in mega cap leaders such as AMZN, FB, GOOGL, MSFT and NVDA, looks to be the start of a new uptrend higher, although there will be pullbacks along the way. (4/2021)

- High quality, lower valuations, current earnings, GARP: Our view is that the market has moved it’s focus to higher quality stocks, at more reasonable valuations, that can generate profits today, both in tech/growth and outside as well. (4/2021)

- Former growth and momentum leaders that have broken down on their charts, could offer big shorter-term trading opportunities, but the longer-terms chart are weaker. (TDOC, PTON, FSLY, etc.) (3/2021)

- It is important to remember, that all of our views here are based on a full reopening of the economy, without any setbacks. (10/2020)

- We think the best approach here is a combination of high quality growth & cyclicals names, plus some exposure to lower volatility sectors, (healthcare, select staples) all in uptrends, slightly higher cash and wider stops based on market volatility. (5/21)

WEEKLY SECTOR SUMMARY & PREVIEW

- Notably improving sectors and industries: Energy, gold miners, healthcare and select consumer defensive (staples) stocks.

- The Financials sector has the most consistent uptrends.

- We think that energy and materials both have the highest potential upside from here, based on current charts. They are also much more volatile.

- Semiconductors led on the week at +2%, and had a favorable earnings report from AMAT – some follow through in this industry would be ideal.

- Travel, airlines, cruise lines and resorts/lodging are also higher R/R ideas, as healthcare news improves.

- Consumer defensive (staples) moved into the top 10 sectors list.

- Retail did not follow through last week, and the markets may be starting to factor in the phase out of additional unemployment stimulus.

- Gold and miners are also a higher potential return vs risk idea here.

SUMMARY

- None of the major U.S. indices made a new high last week, although NDX/QQQ did snap it’s 4-week down streak.

- Markets still appear to be sorting through the high daily flow of economic data and healthcare data.

- Over the past two weeks, the markets have worked through surprise CPI & employment reports and a 50% drawdown in Bitcoin, including a 30% one day drop last week – through that, SPX closed -1.95% off of all-time highs.

- There also has been encouraging earnings data and also favorable healthcare developments.

— - We think that moderation is still key here, across multiple sectors – and not going “all in” on just one.

- Longer-term, cyclicals are still set up very well, in many clean uptrends and continued base breakouts.

- From last Sunday: “Higher valuation/speculative stocks are still in longer term downtrends. They could have very sharp bounces, as discussed since March, but we are avoiding new positions in stocks below the declining 50-sma, or 200-sma, in many cases.” – Leading large cap performers last week included more speculative TUYA, APP, ENPH, SEDG and PLUG, which were all down significantly on the year going into last week. TAN was the leading tracking ETF, but is still -23% ytd.

— - Our view remains that the market has moved it’s focus to higher quality stocks, at more reasonable valuations, that can generate profits today.

- Cyclicals in uptrends, especially financials, industrials, and materials stand out. Energy is improving, but can be more volatile.

- In growth and tech, we favor both the lower valuation stocks in computer hardware, telecom equipment and semis, as well as higher quality, profitable, growth stocks at moderate valuations.

- We think that FB and GOOGL are standout FANG stocks here, and are attractive both technically and due to their ability to grow revenues and profits at reasonable valuations.

— - I’m currently at 13% cash.

- Overall, from a technical perspective, the longer-term charts are constructive and set up well in uptrends here.

- This is still a very news driven and data driven market, so volatility and pullbacks can happen at any time.

- One of the best ways to offset volatility, for those who are trying to mitigate it, is with higher cash and possibly smaller positions.

- We continue to think that the best approach here is a combination of high quality growth & cyclical names, plus some exposure to lower volatility sectors, all in uptrends, slightly higher cash and wider stops based on market volatility.

—

Have a great week,

Larry Tentarelli

Publisher

OPEN POSITIONS

ADDITIONAL CHARTS COVERED IN TODAY’S VIDEO: