There are a few major signs of a potential bottoming process in SPX, as outlined below. A bottoming process does not necessarily mean straight up, new highs soon or that stocks can’t pullback at any time. It does mean no new pullback lows.

The data in the post below is very similar to prior major market lows. That said, we are in an outlier period with the global tariff negotiations. If global economies avoid a recession or not will probably be a key factor that determines if we have seen final lows, or just a short-term low.

We continue to expect very wide trading ranges and continued news driven high-volatility.

It is important to note that the two BofA FMS oversold data points below are much more relevant when combined with last week’s SPX weekly price signal.

4/15/25

Two constructive updates to add today:

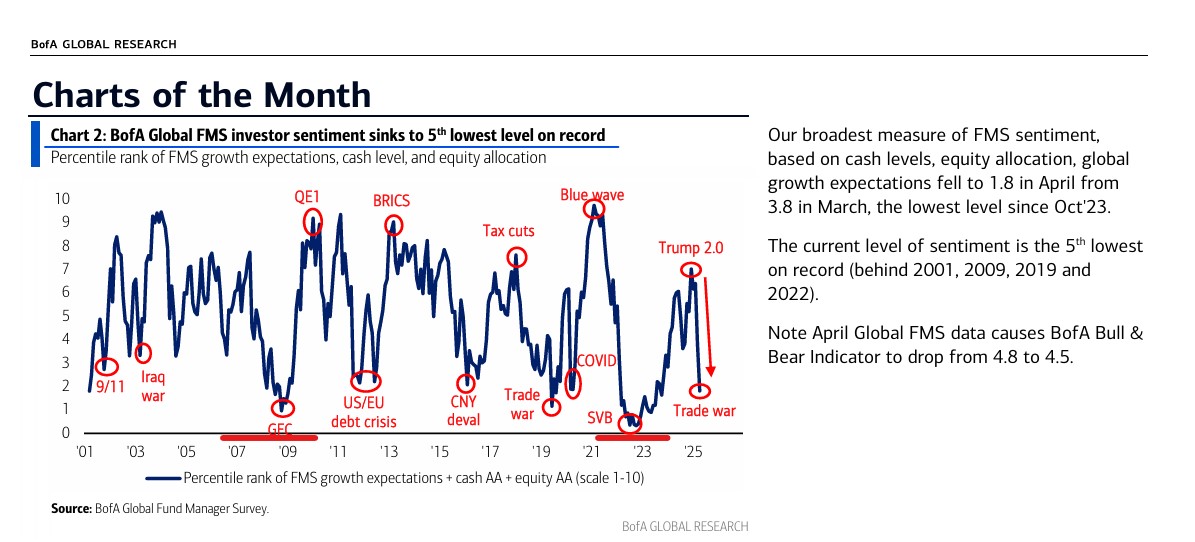

“BofA Global FMS [Fund Manager Survey] investor sentiment sinks to 5th lowest level on record”.

<My take: Other notable low levels were near the GFC and 2022 SPX lows>

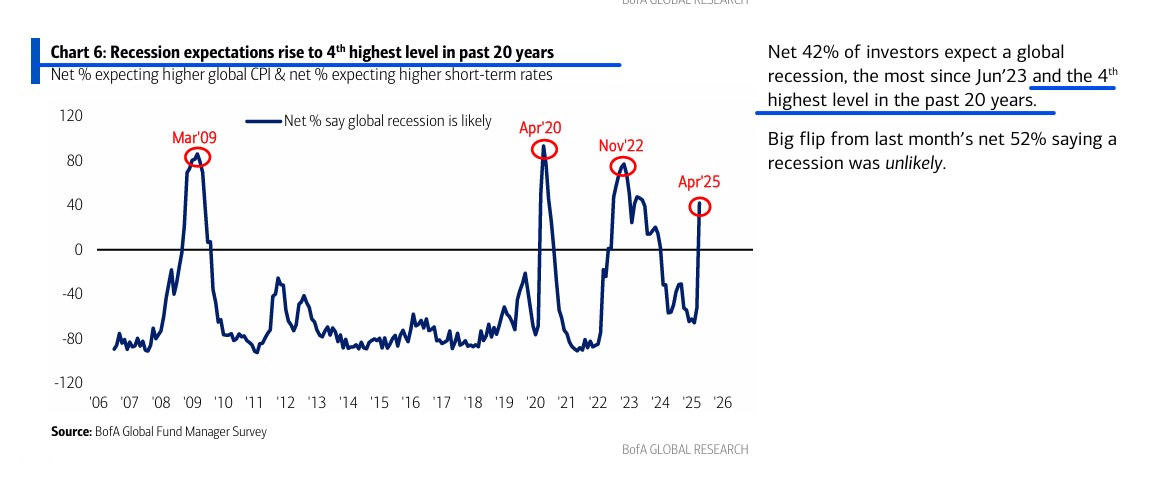

“Net 42% of investors expect a global recession, the most since Jun’23 and the 4th highest level in the past 20 years”.

<My take: Other peaks were at the 09, 20, and 22 market lows. That being said, I expect some type of global economic slowdown too. At other major market lows, there was mostly global Central Bank intervention to turn markets up – right now we have somewhat of the opposite with the trade tariff negotiations>.

4/13/25

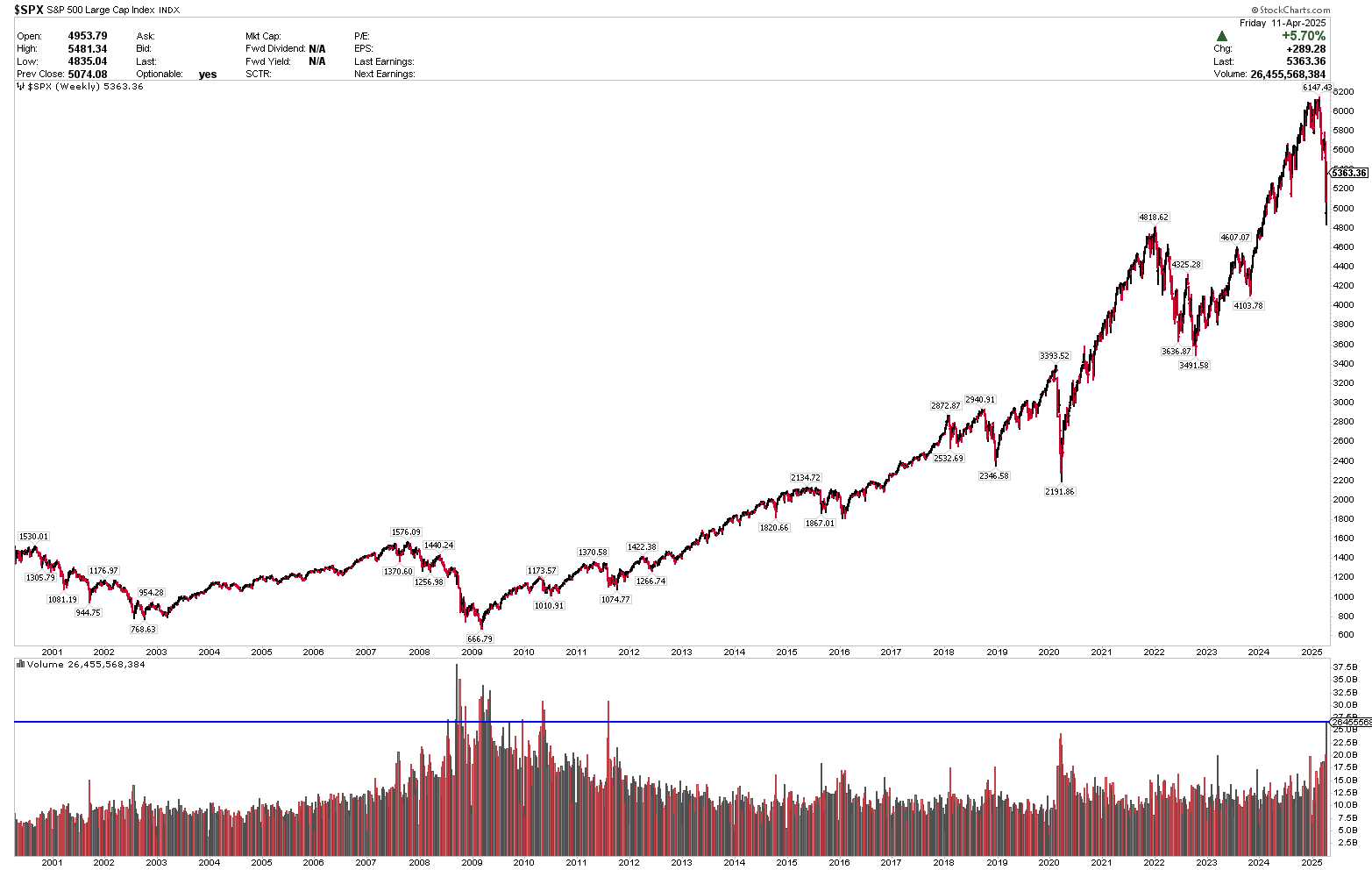

The S&P 500 index just put in the highest weekly volume in 14 years.

- Similar volume spikes in 2009, 2010, 2011 and 2020 marked major market lows. On a technical level, this week’s massive volume selling flush and reversal is identical to prior major market lows. Only 2008 broke lower.

- From a technical perspective, this is an extremely bullish development, as extreme volume selling flushes and reversals often signal major bear market lows.

- From a fundamental perspective, we still have concerns about the volatility of the tariff news cycle and potential economic uncertainty.

- That being said, we believe that the White House is very focused on how the markets will react going forward and we expect the tone of the tariff news cycle could be walked back to a degree. The 90-day tariff pause announced on Wednesday is indicative of this.

- To be clear, I follow price and trends, but I rarely make long-term predictions. This post is not a prediction on my end that a long-term low is in place.

- The high volume selling flush and reversal, into deeply oversold markets is indicative of prior bottoming events.

Another major development is that the Fed has publicly stated now that they will intervene if financial markets show undue stress.

This is in contrast to Jerome Powell’s commentary the prior Friday. We expect that this is related to credit and FX markets, not necessarily stock market volatility. Boston Fed President Susan Collins told the Financial Times: …“We have had to deploy quite quickly, various tools” she told the Financial Times, referring to past interventions to address chaotic conditions in markets. “We would absolutely be prepared to do that as needed.”

One of our major concerns over the past week was that stock market volatility would carry over into the much more important credit and FX markets. This was evident very early Wednesday morning with outsized moves in the bond market. The White House stated this week that bond market volatility was a factor in President Trump’s 90-day tariff pause decision. We believe that both the 90-day tariff pause and Fed backstop will remove some of the major systemic risk concerns from the markets going forward.