Note: This post was released as a Members Only Blog on 5/11/23.

5/11/23

Our Newsletter target cash balance is moving down to a 25-35% target, over the next 4 weeks.

This is based on a few key factors:

1. S&P 500 Index (SPX) and Nasdaq 100 Index (NDX) are both trading over rising 50 & 200-day moving averages.

2. (NDX) made a new 2023 high yesterday.

3. Technology sector ETF (XLK) made a new 52-week high yesterday.

4. 172 of 767 large cap stocks are within 5% or less of new 52-week highs.

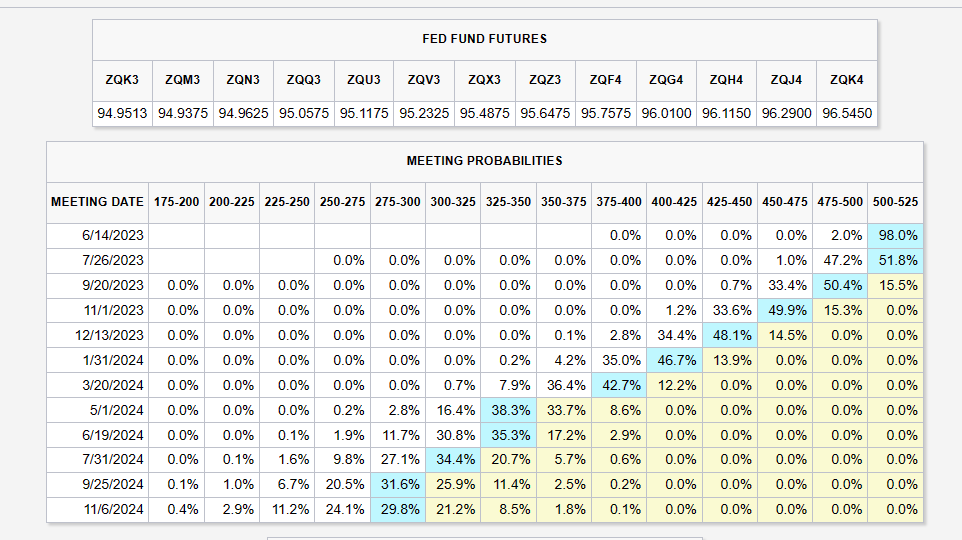

5. The Federal Reserve Open Market Committee (FOMC) has likely reached the end, or near end, of their aggressive rate hiking cycle. The Fed Funds Futures market is pricing in no more rate hikes for this cycle. We anticipate there could be one more hike left, but probably zero. (graph below)

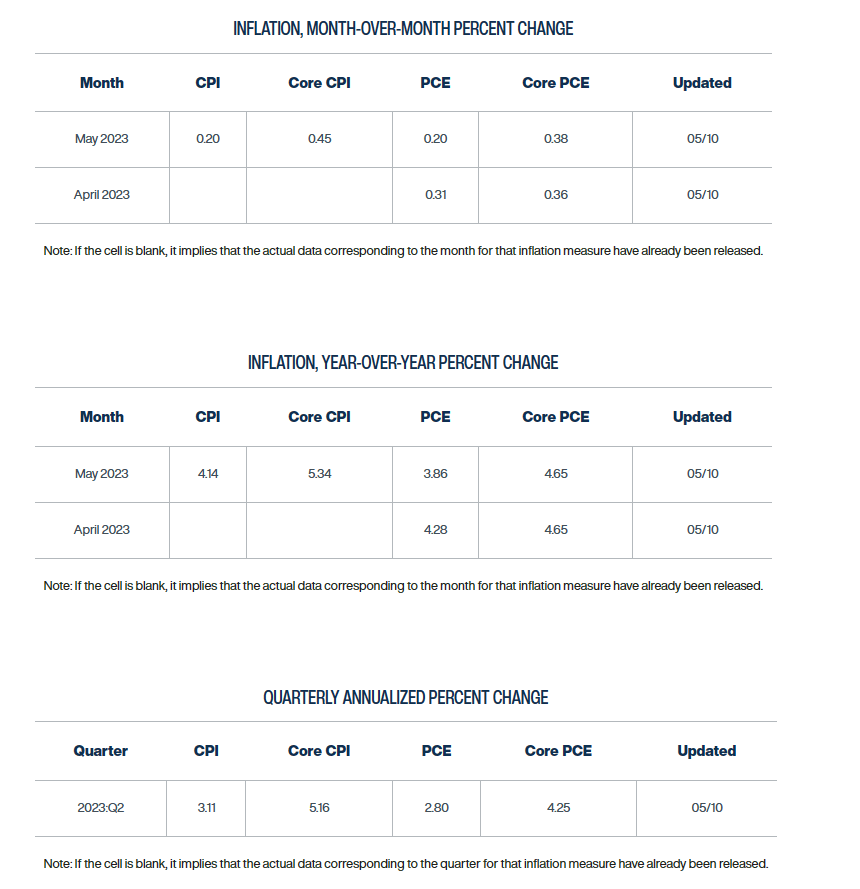

6. Inflation as measured by CPI and PPI is trending lower. Still elevated at 4.9% headline CPI, but trending lower. “Core” inflation is higher, but also trending lower. (graph below)

7. First quarter corporate earnings have mostly been reported (598 of 767) and market reaction overall has been positive.

Risks include:

A potential economic slowdown.

Debt-ceiling market volatility, which we believe will be resolved.

Any increase in regional banking or financial sector stress/failures.

Top ranked sectors/industries currently are:

Technology

Communication Services

Healthcare

Consumer Staples

Gold and Gold miners

Home Construction

Europe and EAFE Index

Select Consumer Discretionary

US Treasury Bonds

Underweight sectors/industries include:

Many cyclicals

Basic Materials

Energy

Financials

The above rankings are subject to change at any time.

This is not a short-term market call. We continue to expect wide ranges, higher-volatility and pullbacks at any time.