This page will be updated every Sunday by 5 PM ET with our weekly outlook and positioning.

5/25/25

WEEKLY TREND OUTLOOK

(1). Both indices pulled back on the week, in what we view as a standard consolidation currently. The S&P 500 index (SPX) closed -2.61% for the week. The Nasdaq 100 index (NDX) closed -2.39% for the week.

(2). Both indices are trading over a rising 40-week moving average (MA), which indicates a long-term uptrend. The 10-week MA is also rising, which indicates an intermediate-term uptrend.

(3). A 2-5% standard pullback for SPX would be the 5848-5670 range, SPX closed Friday at 5802. There is an open price gap and support at 5695-5700. I believe the pullback will be buyable, but I’d want to see TNX stay under 4.80. We discussed a potential index consolidation over the last week, including here, here and here.

(4). The SPX recovery move over 27 days, from April 8 to May 16, was one of the 15 biggest 27-day rallies on record. Historically, these rallies of this magnitude have an almost 100% probability of SPX being higher in 3-6-12 months, post here.

(5). This is still a news-driven, high volatility market, but daily volatility has subsided to a degree. Investors should still expect 1-2% daily ranges are possible, based on news flow.

(6). As has been our view since 4/9/25, we believe that standard pullbacks will be buyable, barring any major outlier news in the tariff cycle, FOMC or economic data/jobs market.

BIGGEST RISKS TO U.S. MARKETS CURRENTLY

SUMMARY:

Technically bullish over rising 10 and 40-week moving averages for SPX and NDX. Markets still need to work through a high volatility news cycle, including tariffs, inflation and the economy. Pullbacks over rising MAs should be buyable. I would like to see index pullbacks stay in the 2-5% range. Nvidia (NVDA) earnings this week could be a major factor.

POSITIONING

5/18/25

SUMMARY:

Technically bullish. Markets still need to work through a high volatility news cycle, including tariffs, inflation and the economy. Pullbacks over rising MAs should be buyable. I would like to see index pullbacks stay in the 2-5% range.

POSITIONING

5/12/25

SPECIAL UPDATE:

The U.S. and China announced a 90-day tariff pause. The S&P 500 index (SPX) and Nasdaq 100 index (NDX) both reclaimed the 200-day moving average today.

Based on today’s news and close, target cash allocation is taken down to 5%.

We are upgrading cyclical sectors (basic materials, consumer discretionary, financials and industrials) and downgrading the overweight in defensive sectors (consumer staples and select lower volatility stocks).

MAXIMUM TARGET ALLOCATIONS

<Updated after the market close on 5/12/25>

Note: These are our target maximum allocations. They are subject to update based on the news cycle.

This does not include all equity sectors, and it is not intended to total 100%.

These are our high-end target limits.

SECTOR/ASSET ALLOCATION

Equal to Overweight sectors:

Neutral to Underweight sectors:

*************************************************************************************

5/11/25

WEEKLY TREND OUTLOOK

S&P 500 Index (SPX):

Potential long-term bottoming process underway.

(1). SPX -0.47% week and NDX – 0.20% week both closed slighter lower for the week and just below the 40-week moving average.

(2) Both made a higher high and a higher low for the week and completed a bullish 4/10-weekly moving average cross.

(3) Both remain in a potential recovery phase. A close soon over 5800 for SPX and over 20500 for NDX would be considered a ‘green light’ signal that the April 7 market lows are likely the lows for this cycle.

(4) Reminder, a Zweig Breadth Thrust was triggered in the NYSE on Thursday [4/24/25], data below. There is a very bullish breadth reversal signal with a 100% success ratio 6 and 12-months forward. More details here.

(5) As noted here last week: “The NDX McClellan Oscillator at 98.96 is the highest level (most overbought) since March 2023. Overbought is considered a sign of market strength, but some index consolidation in the 3-5% range over the next 1-10 days would not be uncommon”.

NDX had a 2.47% drawdown on the week, which is moderate and a continued sign of strength.

(6) This is still a news-driven, high volatility market, but daily volatility has subsided to a degree. Investors should still expect 1-2% daily ranges are possible, based on news flow.

(7) As has been our view since 4/9/25, we believe that standard pullbacks will be buyable, barring any major outlier news in the tariff cycle, FOMC or economic data/jobs market.

(8) U.S./China trade negotiations are scheduled to start tomorrow. This could lead to heightened volatility, in either direction, based on the developments.

Key items of note this coming week: (1) U.S./China trade negotiations. (2) April CPI (Consumer Price Index) is reported on Tuesday and April PPI (Producer Price Index) is reported on Thursday, both at 8:30 AM.

Key items last week:

Focus list sectors: Select technology sector and growth stocks over the 50 and 200-day moving averages, gold, select low volatility/high dividend, defensive stocks in staples, healthcare, utilities and telcos. Bitcoin and related stocks. Cyclical stocks improved last week, in banks, industrials and consumer discretionary. Their rating is under review this week.

Nasdaq 100 “Magnificent 7” Stocks: Neutral, but possibly improving. Two of the seven closed above the 40-week MA, Meta Platforms (META) and Microsoft (MSFT). Tesla (TSLA) is testing the 40-week MA and remains our favorite potential upside idea in this group. All except Nvidia (NVDA) have reported quarterly earnings.

US Treasury Market/Bonds: Neutral. In a trading range below the 40-week MA. Could benefit if the economy slows down, but inflation concerns from tariffs have been a negative headwind for bond prices.

Gold: Buy/accumulate. Long-term uptrend. Spot Gold made the highest weekly close on record, at $3332—. We expect that Gold will continue to work in this tariff cycle, but any positive developments in the tariff cycle could lead to higher volatility.

Crude oil: Neutral to avoid. Weekly downtrend below the 40-week MA. Counter-trend bounces are possible.

Bitcoin: Buy/accumulate. Bitcoin cleared our $90K breakout level on 4/22/25, which generated a new buy signal. It closed Friday 4 PM over $103,000.

Fed rate cut outlook: The Fed funds futures market is pricing in 59.2% odds of a 25-bps rate cut at the 7/30/25 Fed meeting. As of 5/9/25 at 4 PM ET.

SUMMARY:

We continue to add equity exposure, since April 9, with an improving technical outlook. Our technical view is that the extreme volume selling flush and reversal in the week ending 4/11/25 is similar to how other bear markets have ended. The NYSE Zweig Breadth Thrust on 4/24/25 is a major technical event that we do pay attention to. Investors should continue to expect wide daily ranges or headline related pullbacks, but with the VIX under 30, volatility is starting to subside. Markets still need to work through a very high volatility news cycle, including tariff, inflation and the economy. A close over 5800 for SPX and 20500 for NDX would be bullish trend signals.

POSITIONING

***********************************************************************************

5/4/25

S&P 500 Index (SPX):

Potential long-term bottoming process underway.

(1) Our post from 4/11/25, here, that the massive volume reversal week ending 4/11/25 resembled other major bear market lows, continues to hold.

(2) The S&P 500 index (SPX) and Nasdaq 100 index (NDX) both closed over the 10-week moving average on Friday, which is a bullish weekly trend signal.

(3) Both SPX and NDX have recouped all losses from the April 2 tariff announcements.

(4) Reminder, posted here, in last Sunday’s Weekly Trend Report: A Zweig Breadth Thrust (data below) was triggered in the NYSE on Thursday [4/24/25]. There is a very bullish breadth reversal signal with a 100% success ratio 6 and 12-months forward. More details here.

(5) The NDX McClellan Oscillator at 98.96 is the highest level (most overbought) since March 2023. Overbought is considered a sign of market strength, but some index consolidation in the 3-5% range over the next 1-10 days would not be uncommon.

(6) This is still a news-driven, high volatility market. Investors should continue to expect headline related volatility in the 2-3% range, either direction, at any time.

(7) As has been our view since 4/9/25, we believe that standard pullbacks will be buyable, barring any major outlier news in the tariff cycle, FOMC or economic data/jobs market.

(8) Many of our top-ranked stocks appear to be extended, on a near-term basis.

Key items last week:

Focus list sectors: Select technology sector and growth stocks over the 50 and 200-day moving averages, gold, select low volatility/high dividend, defensive stocks in staples, healthcare, utilities and telcos. Bitcoin and related stocks.

Nasdaq 100 “Magnificent 7” Stocks: Neutral, but possibly improving. Two of the seven closed above the 40-week MA, Meta Platforms (META) and Microsoft (MSFT). All except Nvidia (NVDA) have reported quarterly earnings.

US Treasury Market/Bonds: Neutral. In a trading range below the 40-week MA. Could benefit if the economy slows down, but inflation concerns from tariffs have been a negative headwind for bond prices.

Gold: Buy/accumulate. Long-term uptrend, but pulling back over the past two weeks. We expect that Gold will continue to work in this tariff cycle, but any positive developments in the tariff cycle could lead to a pullback for Gold.

Crude oil: Neutral to avoid. Weekly downtrend below the 40-week MA. Counter-trend bounces are possible.

Bitcoin: Buy/accumulate. Bitcoin cleared our $90K breakout level, which generated a new buy signal.

Fed rate cut outlook: The Fed funds futures market is pricing in 34.9% odds of a 25-bps rate cut at the 6/18/25 Fed meeting.

Key items of note this week: (1) The FOMC decision and press conference, this Wednesday. (2) Corporate earnings reports.

SUMMARY:

We continue to add equity exposure, since April 9, with an improving technical outlook. Our technical view is that the extreme volume selling flush and reversal in the week ending 4/11/25 is similar to how other bear markets have ended. The NYSE Zweig Breadth Thrust on 4/24/25 is a major technical event that we do pay attention to. Investors should continue to expect wide daily ranges or headline related pullbacks, but with the VIX under 30, volatility is starting to subside. Markets still need to work through the corporate earnings cycle and the unknown effects of this tariff cycle on the economy and labor markets. The NDX McClellan Oscillator at 98.96 is the highest level (most overbought) since March 2023. Overbought is considered a sign of market strength, but some index consolidation in the 3-5% range over the next 1-10 days would not be uncommon.

POSITIONING

MAXIMUM TARGET ALLOCATIONS

Updated weekly current as of 5/4/25

Note: These are our target maximum allocations. They are subject to update based on the news cycle.

This does not include all equity sectors, and it is not intended to total 100%.

These are our high-end target limits.

***********************************************************************************************************

WEEKLY TREND OUTLOOK

4/27/25

S&P 500 Index (SPX):

Potential long-term bottoming process underway.

(1) Our post from 4/11/25, here, that the massive volume reversal week ending 4/11/25 resembled other major bear market lows, continues to hold.

(2) Other bullish price signals this week were that SPX and NDX both made higher weekly highs and higher weekly lows vs the 4/11/25 recovery week.

(3) A Zweig Breadth Thrust was triggered in the NYSE on Thursday. There is a very bullish breadth reversal signal with a 100% success ratio 12-months forward. More details here.

(4) SPX closed the week over 5500, which is a key technical resistance level. Post here.

(5) There is a “Trump Put” in the markets at SPX 4800-5100. We saw that with the 4/9/25 90-day tariff pause and 4/22/25 slight walk back of the China tariff and Jerome Powell narratives.

(6) With Tuesday’s China tariff slight walk back by the White House and subsequent market reaction, our defensive sectors overweight has been rescinded.

Key SPX factors going forward:

Our technical view that the 4/7/25 lows at 4835 should hold will be based primarily on three factors:

(1) No major regression in the global trade tariffs talks. No walk back of the 90-day tariff pause. No major escalation vs China.

(2) No major corporate earnings misses or major guidance downgrades over the next few weeks, especially in the Nasdaq 100 mega cap leaders.

(3) That the U.S. economy avoids a recession or major slowdown in 2025 and that the U.S. labor markets stay strong.

There are always other outliers, including inflation, but these are the three data points that we are most focused on.

Expect daily volatility ranges of 2-3% at any time. SPX is more cautionary below the 40-week moving average.

Focus list sectors: Select technology sector and growth stocks over the 50 and 200-day moving averages, gold, gold miners, select low volatility/high dividend, defensive stocks in staples, healthcare, utilities and telcos. Bitcoin and related stocks.

Nasdaq 100 “Mag 7” Stocks: Neutral, but possibly improving. All seven are below the 40-week moving average currently, but had strong weeks.

US Treasury Market/Bonds: Neutral. In a trading range below the 40-week MA. Could benefit if the economy slows down, but inflation concerns from tariffs have been a negative headwind for bond prices.

Gold: Buy/accumulate. Long-term uptrend, new record highs last week.

Crude oil: Neutral to avoid. Weekly downtrend below the 40-week MA. Counter-trend bounces are possible.

Bitcoin: Buy/accumulate. Bitcoin cleared our $90K breakout level, which generated a new buy signal.

Fed rate cut outlook: The Fed funds futures market is pricing in 64.3% odds of a 25-bps rate cut at the 6/18/25 Fed meeting.

Key items of note this week: Corporate earnings reports, (Weds.) GDP, PCE inflation, (Fri.) monthly payrolls report.

SUMMARY:

We continue to add equity exposure, since April 9, with an improving technical outlook. Our technical view is that the extreme volume selling flush and reversal in the week ending 4/11/25 is similar to how other bear markets have ended. The NYSE Zweig Breadth Thrust this week is a major technical event that we do pay attention to. There is a “Trump Put” at SPX 4800-5100 which could provide a floor as well. Investors should continue to expect wide daily ranges or headline related pullbacks, but volatility is starting to subside. Markets still need to work through the corporate earnings cycle and the unknown effects of this tariff cycle on the economy and labor markets.

POSITIONING

MAXIMUM TARGET ALLOCATIONS

Updated weekly current as of 4/27/25

Note: These are our target maximum allocations. They are subject to update based on the news cycle.

This does not include all equity sectors, and it is not intended to total 100%.

These are our high-end target limits.

SECTOR/ASSET ALLOCATION

Equal to Overweight sectors:

Neutral to Underweight sectors:

*****************************************************************************************************************************************************

4/20/25

WEEKLY TREND OUTLOOK

S&P 500 Index (SPX): Potential long-term bottoming attempt underway. If the U.S. avoids a recession will probably determine if the recent low at 4835 holds. A major selling flush and reversal + highest weekly volume in 14 years, the week ending 4/11/25. Expect daily volatility ranges of 2-3% at any time. SPX is more cautionary below the 40-week moving average. Potential wide trading range between 4900-5600. Focus on stock selection.

Sectors to overweight vs the index: Cash, gold, gold miners, select low volatility/high dividend, defensive stocks in staples, healthcare, utilities and telcos.

Sectors to underweight vs the index: High beta technology, cyclicals: energy, industrials, banks.

Nasdaq 100 “Mag 7” Stocks: Underweight. All seven are in weekly downtrends below the 40-week moving average.

US Treasury Market/Bonds: Neutral. In a trading range below the 40-week MA. Could benefit if the economy slows down, but inflation concerns from tariffs have been a negative headwind for bond prices.

Gold: Buy/accumulate. Long-term uptrend, new record highs last week. Possibly extended in the near-term.

Crude oil: Avoid. Weekly downtrend below the 40-week MA. Counter-trend bounces are possible.

Bitcoin: Hold: Above the 40-week MA. In a trading range between 75K – 90K. Potential range breakout if over 90K.

Fed rate cut outlook: The Fed funds futures market is pricing in 61% odds of a 25-bps rate but at the 6/18/25 Fed meeting.

Current positioning: Maintain defensive positioning with SPX below the 40-week MA. Hold extra cash, index hedges, and overweight defensive sectors. Smaller position sizing, scale into any new buys.

SUMMARY:

Our technical view is that the extreme volume selling flush and reversal in the week ending 4/11/25 is similar to how other bear markets have ended. From a fundamental perspective however, there are too many unknows with respect to the tariff news cycle, corporate earnings guidance and if the U.S. economy will enter a notable slowdown or recession. Charts and price data alone cannot predict news flow. This is a unique period in market history, going into global trade negotiations with above target inflation. Based on the uncertainty of the tone and duration of the tariff negotiations and unknown impact on the global economy, we are still maintaining defensive positioning, but with an improving outlook.

POSITIONING

MAXIMUM TARGET ALLOCATIONS

Updated weekly current as of 4/20/25

Note: These are our target maximum allocations. They are subject to update based on the news cycle.

This does not include all equity sectors, and it is not intended to total 100%.

These are our high-end target limits.

SECTOR/ASSET ALLOCATION

Equal to Overweight sectors:

Underweight sectors:

************************************************************************************************************************************

AS OF THE 4/9/25 90-DAY TARIFF PAUSE, ALL INFORMATION BELOW IS UNDER REVIEW.

4/6/25

April 2025 Tariff Investors Guide – Blue Chip Daily Trend Report

The 4/3/25 and 3/2/25 Defensive Rotation blog are below.

4/3/25

Following the U.S. tariff announcements yesterday, which came in higher than forecast, we expect that the markets will continue to rotate into defensive stocks and sectors and out of many cyclicals, high valuation stocks and high beta tech. We don’t expect these to be straight line moves, but this tariff cycle could take some time to develop. I am moving our economic slowdown/recession probability in 2025 up to 50%, from 30%. In this environment, I would expect lower volatility and traditional defensive sectors to outperform (consumer staples, traditional utilities, telecommunication services, and lower volatility healthcare).

Note: This is based on currently available data. If there is a major change in the tariff outlook or narrative, these views could change quickly. Also, markets are trading in very wide ranges. Higher volatility in almost all charts is expected currently.

Gold: From a fundamental view, we expect Gold to remain a beneficiary of global macro uncertainty from a potential tariff trade war. On a technical level, Gold is in a confirmed uptrend, and it is constructive here and on pullbacks. This is a high conviction idea.

Bonds: We expect a notable slowdown in the U.S. economy in 2025, from tariff related concerns. Also, large cuts in U.S. government jobs and large cuts in U.S. government spending. Bonds have not yet broken out in 2025, due to inflation concerns from tariffs, but we expect that they will start to break out shortly. This is a medium conviction idea.

Overweight sectors:

Low volatility, low valuation and/or high dividend

Consumer staples

Traditional utilities

Telecommunication services

Insurance

Lower Volatility healthcare

Gold

Underweight sectors:

High valuation and high beta growth stocks

Technology

Banks

Traditional cyclicals (industrials and consumer discretionary)

Speculative growth stocks

Updated defensive ideas tracking list

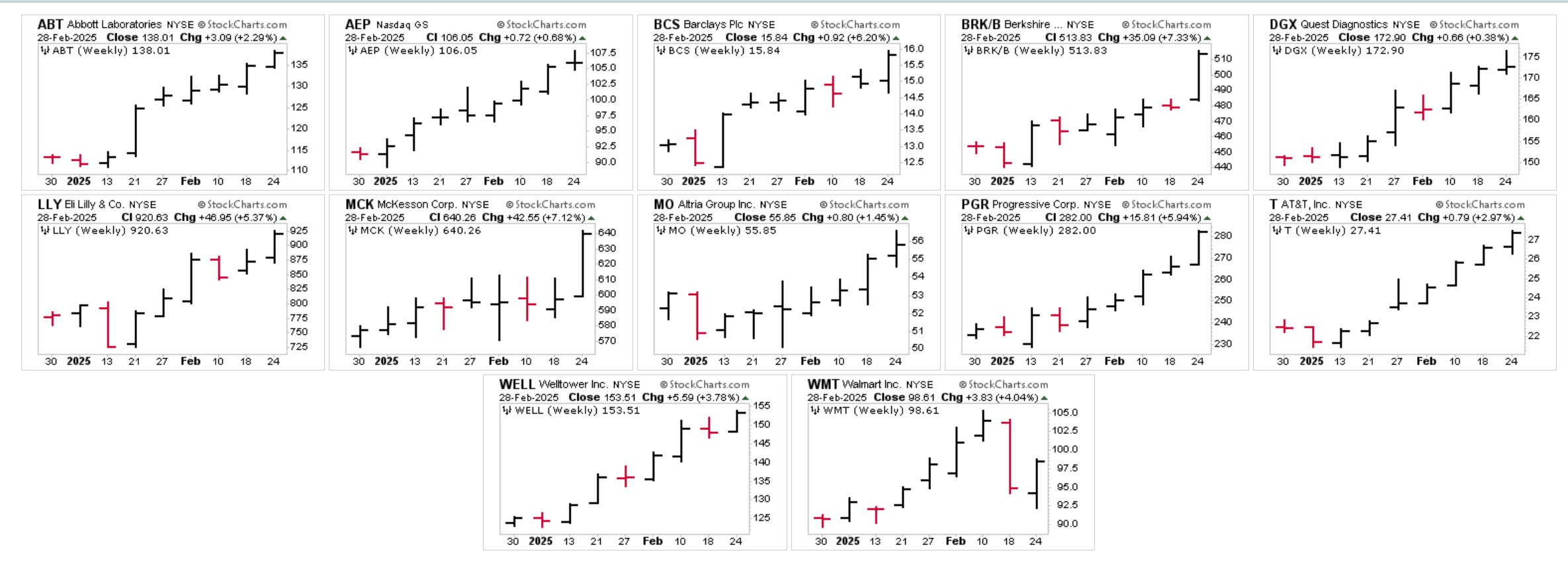

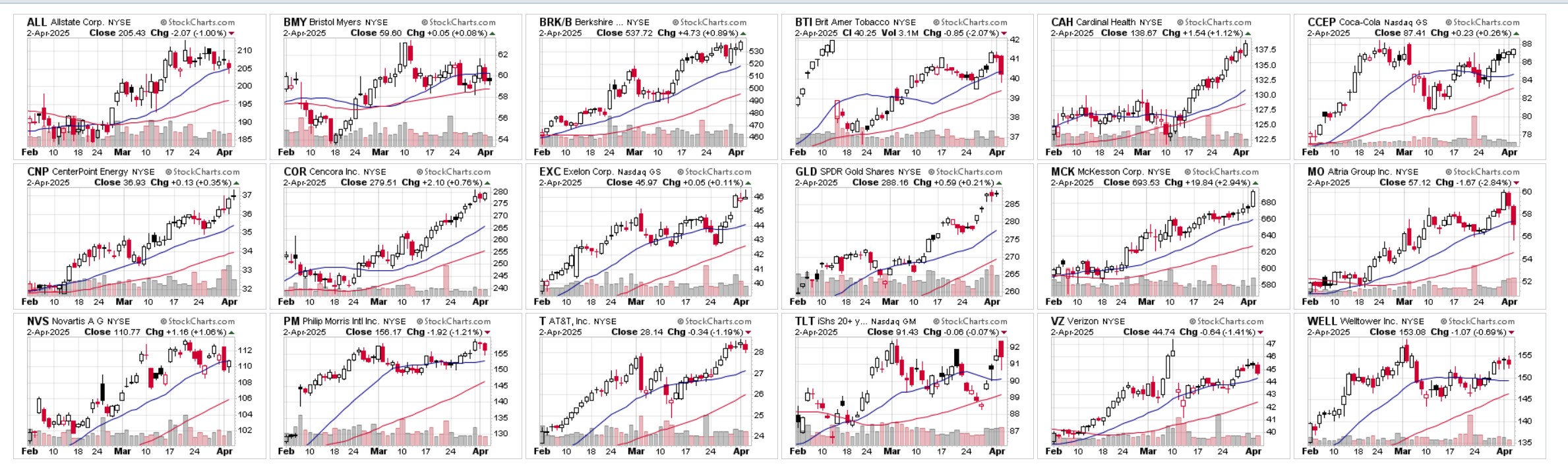

ALL, BMY, BRK/B, BTI, CAH, CCEP, CNP, COR, EXC, MCK, MO, NVS, PM, T, VZ, WELL

GLD, TLT

ORIGINAL MARCH 2, 2025 POST AND VIDEO IS BELOW

3/2/25

VIDEO: https://bit.ly/BCDDefensiveRotationVideo3225

Note: This blog and video discusses the recent market rotation into bonds and traditional defensive sectors in the stock market. There is no assurance on our end that this rotation will continue, but it is something that investors should be aware of and should prepare for, in the event that it does follow through. We saw a similar defensive rotation in mid 2024 that did not follow through.

We have gradually increased defensive and/or lower valuation positions over the past two weeks, and we could raise that exposure if the rotation continues.

WATCH INCOMING DATA

Over the past 7 weeks, there has been a defensive rotation in the markets, highlighted by four keys factors:

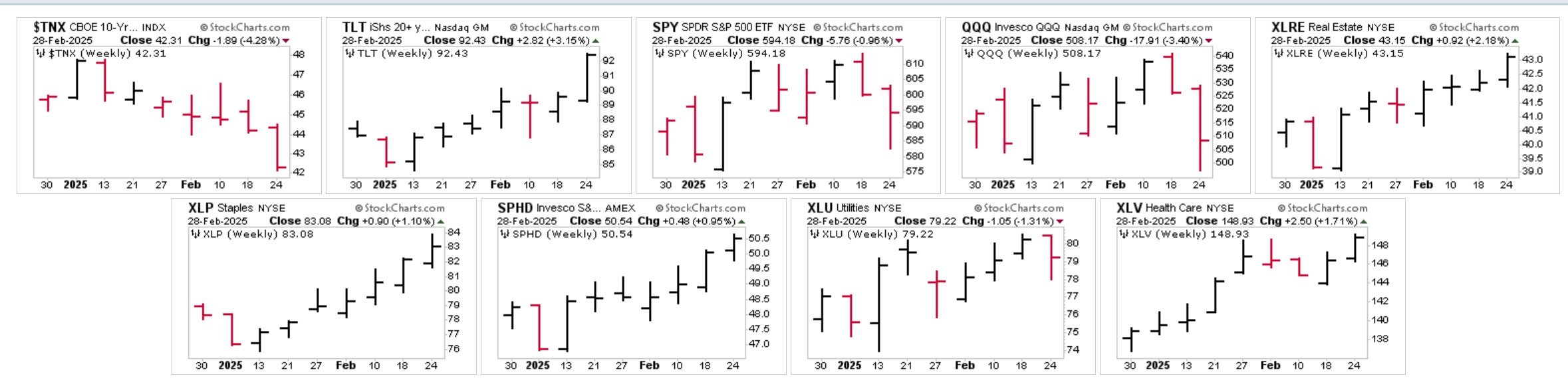

1. 10-year US Treasury Yields (TNX) pulled back by 59 basis points, from a recent peak at 4.80 on January 14, to a recent low point of 4.214 on February 28. TNX closed at 4.231 on Friday, – 57 basis points from the recent high.

2. Bond prices are rising.

3. Defensive sectors in the stock market are outperforming.

4. Low valuation stocks, lower volatility stocks and/or high dividend stocks also tend to perform well in defensive rotations. Low price-to-earnings (PE) ratio stocks often see less valuation compression in slowdowns and high dividends are considered an attractive part of an overall total return.

Returns since the January 13/January 14, 2025, inflection point:

CBOE 10-year UST Yields (TNX) -57 basis points

iShares 20+ year Treasury bond ETF +9.28%

S&P 500 ETF (SPY) +3.27%

Nasdaq 100 ETF (QQQ) +1.69%

SPDR Real Estate ETF (XLRE) +10.49%

SPDR Consumer Staples ETF (XLP) +9.60%

Invesco S&P High Dividend Low Volatility ETF (SPHD) + 8.13%

SPDR Utilities ETF (XLU) +7.86%

SPDR Healthcare ETF (XLV) +7.23%

The above noted charts are shown below, from the beginning of 2025 through Friday’s close.

Select defensive sector ideas: